Milestone Pharmaceuticals (NASDAQ MIST): From Regulatory Success to Commercial Proof

CARDAMYST is approved and clinically validated. The remaining question is whether disciplined execution, payer alignment, and physician adoption can turn a single-asset launch into a durable franchise

Executive Overview

Milestone Pharmaceuticals is no longer a regulatory story. CARDAMYST is approved, manufactured, and ready for launch. The investment question has shifted decisively away from “does it work?” toward a more demanding and ultimately more revealing test: can Milestone translate clear clinical and economic logic into repeatable prescribing behavior?

CARDAMYST is the first FDA-approved, patient-administered therapy for acute PSVT in more than three decades. It moves treatment out of the emergency department and into the hands of patients, addressing a structural inefficiency in cardiovascular care rather than a speculative biological target. The mechanism is familiar. The pharmacology is well understood. The label explicitly permits self-administration and repeat dosing within a single episode.

What remains uncertain is commercial execution.

Milestone’s valuation will be determined by how efficiently commercial spending converts into sustained utilization, how quickly payer access normalizes, and whether early prescriber interest becomes habitual clinical use. This is not a binary biotech outcome. It is a specialty pharma launch with bounded downside, measurable milestones, and asymmetric upside if adoption inflects.

Company Overview

Milestone Pharmaceuticals was founded in 2003 in Montréal, Québec by Joseph Oliveto, who continues to serve as President and Chief Executive Officer. From inception, the company was built around a deliberately narrow and pragmatic vision: rather than operating as a broad discovery platform, Milestone focused on developing a single, clinically meaningful therapy aimed at correcting a clear failure in healthcare delivery. That philosophy has shaped its evolution into a focused, single-product cardiovascular company centered on moving effective treatment out of hospital settings and into the hands of patients.

Unlike many biotechnology companies that pursue optionality through pipeline breadth, Milestone has consistently prioritized execution depth. Its strategy reflects an early recognition that in small organizations, dilution of focus often creates more risk than it mitigates. This willingness to accept concentration risk in exchange for clarity and capital efficiency has defined the company’s trajectory from development through commercialization.

Company History

Milestone was founded with a problem-driven mandate: to enable fast-acting cardiovascular therapies that could be safely and effectively used outside traditional acute-care environments. Management identified that certain arrhythmias were not inadequately treated due to a lack of effective drugs, but because existing therapies were structurally confined to emergency departments and inpatient settings.

Rather than pursuing multiple programs, Milestone committed nearly all scientific, regulatory, and financial resources to a single molecule, etripamil. This decision reflected a strategic choice to maximize the probability of success for one clearly defined solution rather than dilute effort across parallel initiatives.

Early development focused on overcoming two interdependent challenges that historically prevented outpatient treatment of acute arrhythmias. First, etripamil needed to demonstrate rapid enough pharmacokinetics to terminate arrhythmic episodes within clinically meaningful timeframes. Second, the drug required a delivery system that could be safely self-administered during symptomatic distress without medical supervision or intravenous access. Addressing these challenges required not only formulation work, but extensive human-factors validation to ensure real-world usability.

Milestone advanced etripamil through a series of clinical studies that progressively de-risked both efficacy and self-administration. This effort culminated in two pivotal Phase 3 trials, RAPID and NODE-301, which demonstrated that intranasal etripamil significantly increased conversion to sinus rhythm within relevant timeframes compared with placebo in patients with paroxysmal supraventricular tachycardia. These results validated the core therapeutic and workflow hypothesis and formed the basis for the company’s public-market entry as a single-asset biotechnology company.

In early 2025, Milestone received a Complete Response Letter from the FDA. Crucially, the CRL did not raise concerns about clinical efficacy or safety. Instead, it cited chemistry, manufacturing, and controls issues, including facility inspection findings and additional data requests related to manufacturing readiness. This moment marked a critical inflection point. Milestone responded by strengthening quality systems, remediating manufacturing deficiencies, and aligning its operations with commercial-scale regulatory expectations. Following resubmission, the FDA approved CARDAMYST, the branded intranasal formulation of etripamil, in December 2025.

With approval, Milestone transitioned from a development-stage biotechnology company into a commercial-stage cardiovascular pharmaceutical operator. The company’s history reflects a consistent strategic throughline: acceptance of concentration risk, emphasis on practical clinical utility, and steady progression from scientific validation to regulatory execution and commercialization.

Company Philosophy

Milestone’s philosophy is fundamentally pragmatic rather than aspirational, and this distinction is central to how the company should be evaluated. It has never positioned itself as a discovery platform or a pipeline aggregator. Instead, Milestone operates from a clinical-utility-first mindset, identifying situations where patients are pushed into inefficient, costly, and stressful care pathways not because of therapeutic gaps, but because existing solutions are locked inside acute-care settings.

The first principle of this philosophy is solving workflow failures rather than theoretical medical problems. PSVT is not underserved due to lack of pharmacological efficacy; effective therapies have existed for decades. The failure lies in where and when those therapies are administered. By enabling self-administration at symptom onset, Milestone targets the structural mismatch between episodic disease and hospital-based treatment. This workflow-centric thinking underpins the entire CARDAMYST strategy.

The second principle is a deliberate preference for predictability over optionality. From the outset, Milestone chose depth instead of breadth, committing to a single asset, a single primary indication, and a clearly defined regulatory path. This was not a lack of ambition, but a risk-management decision. Management recognized that execution risk often compounds faster than scientific risk when capital, attention, and operational capacity are spread too thin. This philosophy explains both the company’s narrow focus and its willingness to absorb short-term pain, including the 2025 CMC-related delay, to build a more durable operational foundation.

The third principle is designing the business around payer logic rather than hype cycles. CARDAMYST is framed less as a premium innovation and more as a system-level efficiency tool. Its value proposition is rooted in reducing emergency department utilization, shortening episode duration, and improving patient quality of life at a lower total cost of care. By anchoring the product’s narrative to economics and utilization rather than novelty, Milestone positions itself to reduce long-term reimbursement friction and improve formulary acceptance.

Collectively, these principles place Milestone closer to a focused healthcare operator than a speculative R&D venture. Future outcomes will be driven less by scientific surprise and more by execution discipline, payer alignment, and real-world adoption.

Business Model Evolution

Phase 1: Single-Asset Clinical Development

In its earliest phase, Milestone operated as a tightly focused R&D organization built around a single hypothesis: that a fast-acting, self-administered calcium channel blocker could change the treatment paradigm for acute PSVT. The company deliberately avoided platform claims or multi-asset expansion, concentrating resources on de-risking etripamil through late-stage trials.

Value creation during this period was binary. Success depended on demonstrating efficacy, safety, and consistency sufficient for regulatory approval. Commercial considerations were secondary, as no revenue was possible prior to approval. Capital efficiency was achieved through discipline rather than diversification, with reliance on continued access to capital markets to fund operations.

Phase 2: Regulatory Reset and Operational Hardening

The 2025 Complete Response Letter forced a structural transition. While the clinical case remained intact, the CRL exposed gaps in manufacturing readiness and quality systems. Milestone was required to evolve from a trial-focused organization into one capable of supporting a commercial product lifecycle.

This phase required investment in FDA-grade manufacturing oversight, supplier qualification, and scalable quality infrastructure. These efforts did not generate revenue and appeared dilutive in the near term, but they materially reduced existential risk. The company effectively paid an execution tax upfront to ensure that approval, once granted, would be durable rather than fragile.

Phase 3: Commercial-Stage Specialty Pharma

With FDA approval, Milestone enters its third phase as a focused specialty pharmaceutical company. The commercial model remains intentionally narrow: a single product, a single primary indication, and a defined prescriber base of cardiologists and electrophysiologists. Demand creation is education-driven rather than volume-driven, reflecting the need to change behavior rather than compete within an existing prescribing class.

At this stage, growth is constrained not by science, but by execution. Success depends on payer access, physician education, patient adherence, and real-world effectiveness. While label expansion into adjacent acute arrhythmia settings may provide upside, it is optional rather than foundational.

As a result, Milestone is no longer valued on the probability of approval. Its valuation now rests on its ability to translate regulatory success into sustained prescribing behavior, payer acceptance, and predictable revenue growth. The company’s risk profile has shifted from binary regulatory outcomes to continuous operational performance.

Management and Leadership Analysis

Executive Management

Milestone Pharmaceuticals is led by an executive team whose experience is concentrated in late-stage development, regulatory execution, and specialty pharmaceutical commercialization rather than early-stage discovery science. This leadership profile is not incidental. It reflects the company’s strategic decision to remain narrowly focused on a single asset and a single primary indication, and it aligns closely with Milestone’s transition from a development-stage biotechnology company into a commercial-stage specialty pharmaceutical operator.

Collectively, the management team emphasizes regulatory credibility, operational discipline, and execution over pipeline expansion or platform ambition. This orientation became more pronounced following the company’s regulatory setback in early 2025, which underscored the importance of manufacturing readiness, quality systems, and commercial-grade operational rigor. The current leadership composition is therefore best understood as execution-centric rather than visionary, optimized for navigating commercialization risk rather than scientific exploration.

Joseph G. Oliveto — President and Chief Executive Officer

Joseph Oliveto serves as President and Chief Executive Officer and is a member of the Board of Directors. He has led Milestone since 2017 and has been the central executive figure throughout the company’s most consequential phases, including late-stage clinical development, regulatory engagement with the FDA, remediation following the Complete Response Letter, and preparation for commercial launch.

Oliveto brings deep experience from the specialty pharmaceutical sector, most notably from his tenure as President and CEO of Chelsea Therapeutics International, where he oversaw late-stage development, regulatory interactions, and strategic execution during a period of organizational transition. Earlier roles at Roche exposed him to global pharmaceutical operations, alliance management, and disciplined portfolio execution. This background has shaped a leadership style centered on regulatory credibility, operational rigor, and capital discipline rather than pipeline breadth.

At Milestone, Oliveto consistently prioritized focus over optionality. He resisted pressure to pursue parallel programs or platform narratives that could dilute organizational capacity. This discipline proved critical during the 2025 CRL, which stemmed from manufacturing and quality system deficiencies rather than clinical shortcomings. Oliveto led the remediation effort, reallocating resources toward operational hardening and regulatory compliance, ultimately securing approval and preserving long-term asset value.

As Milestone enters its commercial phase, Oliveto’s role shifts from development oversight and capital markets navigation to execution accountability. His leadership will now be judged on launch discipline, payer access outcomes, and the company’s ability to convert regulatory success into sustained prescribing behavior and shareholder value.

Amit Hasija — Chief Financial Officer and EVP of Corporate Development

Amit Hasija serves as Chief Financial Officer and Executive Vice President of Corporate Development, placing him at the center of Milestone’s financial stewardship and strategic optionality as the company transitions into commercialization. His responsibilities span financial planning and reporting, capital structure management, investor relations, and corporate development initiatives.

As Milestone evolves beyond predictable R&D spending into a launch environment characterized by front-loaded commercial investment and delayed revenue realization, Hasija’s role has expanded materially. He is responsible for managing uneven cash flows, prioritizing commercial expenditures, and sequencing capital deployment to preserve runway while limiting dilution.

Hasija plays a central role in evaluating financing alternatives, including equity, debt, and royalty-based structures, with an emphasis on extending operational flexibility without compromising long-term value. His oversight ensures that capital is directed toward initiatives with the highest near-term impact on launch execution, including market access preparation, sales force readiness, and supply continuity.

In his corporate development capacity, Hasija also evaluates partnership opportunities and lifecycle extensions for etripamil, acting as a constraint on overextension. His effectiveness will be reflected in cash burn discipline, dilution management, and Milestone’s ability to sustain commercialization long enough for CARDAMYST to demonstrate durable real-world adoption.

David B. Bharucha, M.D., Ph.D., FACC — Chief Medical Officer

Dr. David Bharucha serves as Chief Medical Officer, providing medical and clinical leadership as Milestone transitions from development into commercialization. His remit includes oversight of clinical strategy, medical affairs, post-approval safety surveillance, and medically focused regulatory interactions.

As CARDAMYST moves from controlled trial settings into broader patient populations, Dr. Bharucha’s role is central to pharmacovigilance, real-world evidence generation, and ensuring alignment between observed outcomes and the approved label. He also plays a critical role in external scientific engagement, interfacing with cardiologists, electrophysiologists, and key opinion leaders to contextualize clinical data and support appropriate patient selection.

His dual medical and scientific training lends credibility with both regulators and clinicians, reinforcing confidence in the product as it enters routine clinical practice. Dr. Bharucha’s leadership helps ensure that medical rigor remains tightly integrated with commercial execution, reducing long-term risk and supporting sustainable adoption.

Lorenz Müller — Chief Commercial Officer

Lorenz Müller serves as Chief Commercial Officer and is responsible for building and executing Milestone’s commercial strategy for CARDAMYST. His mandate spans market access, sales organization design, pricing and reimbursement strategy, and coordination across sales, marketing, and medical affairs.

CARDAMYST presents a structural commercialization challenge. It requires physicians to alter established acute-care workflows and proactively identify patients suitable for self-administration. Accordingly, Müller’s approach emphasizes education, workflow integration, and targeted engagement rather than broad promotional scale.

He is also responsible for securing payer coverage and minimizing reimbursement friction by aligning the product’s value proposition with payer priorities such as emergency department avoidance and reduced healthcare utilization. Early success in market access will be a key determinant of prescription velocity and persistence.

Müller oversees the build-out of a right-sized commercial infrastructure, balancing productivity with capital discipline. His performance will be judged on prescriber activation, payer access breadth, and sustained utilization rather than headline launch metrics.

Jeffrey Nelson — Chief Operating Officer

Jeffrey Nelson serves as Chief Operating Officer and is responsible for translating Milestone’s regulatory and strategic achievements into a stable operating platform. His remit includes supply chain readiness, third-party manufacturing coordination, quality systems integration, and cross-functional execution.

Nelson’s internal continuity, developed through prior senior operational roles at Milestone, has been particularly valuable during regulatory remediation and launch preparation. He oversees manufacturing partners, ensuring regulatory compliance, commercial supply reliability, and scalable quality oversight.

As Milestone enters its first commercial cycle, Nelson’s role is execution-critical. While revenue generation depends on commercial success, the durability of that revenue depends on operational stability, an area squarely under his oversight.

Roshan Girglani — Vice President of Marketing

Roshan Girglani leads marketing strategy for CARDAMYST, with responsibility for brand positioning, messaging architecture, and educational frameworks that support prescribers, payers, and patients. In this context, marketing is instructional rather than promotional, focused on enabling correct patient identification and use.

Girglani brings experience from specialty and hospital-adjacent pharmaceutical launches, with a background in cross-functional coordination across medical affairs, market access, and sales. At Milestone, he is responsible for ensuring that clinical, economic, and workflow narratives are coherent and aligned.

His effectiveness will be measured by clarity of communication, consistency across channels, and the extent to which marketing supports sustained prescribing behavior rather than short-term awareness.

Jeff Moore — Vice President of Sales

Jeff Moore leads Milestone’s field sales organization and is responsible for converting clinical approval into repeat prescribing behavior among a targeted physician base. His mandate emphasizes disciplined territory design, account prioritization, and alignment with medical and market access functions.

Early launch success under Moore’s leadership will be measured not simply by prescription volume, but by prescriber activation depth, repeat utilization, and durability of adoption within priority accounts. His role is central to determining whether CARDAMYST transitions from early interest to embedded clinical practice.

Board of Directors

Milestone’s Board of Directors reflects a deliberate shift toward governance aligned with commercialization execution, capital discipline, and risk oversight. The board is composed primarily of independent directors with deep experience in pharmaceuticals, finance, and healthcare governance.

The board is chaired by Robert J. Wills, Ph.D., an independent non-executive director with over three decades of industry experience spanning scientific, commercial, and governance roles. His leadership provides stability as Milestone navigates its transition into revenue generation.

Recent board refreshment has strengthened financial and commercial oversight. Stuart Duty brings extensive investment banking and biotech advisory experience.

Andrew Saik contributes deep financial stewardship expertise from CFO roles in growth-stage biopharma.

Seth Fischer adds operational industry perspective, and Lisa M. Giles contributes governance and compliance experience across healthcare companies.

The appointment of Joseph Papa in September 2024 adds significant commercial and M&A experience. Papa’s background as CEO and chairman of multiple global healthcare companies is directly relevant as Milestone seeks to establish CARDAMYST as a sustainable franchise.

Joseph Oliveto’s presence on the board ensures alignment between execution realities and strategic oversight. Overall, the board composition reflects a governance posture focused on disciplined growth, accountability, and long-term value creation rather than promotional ambition.

Corporate Structure

Milestone Pharmaceuticals operates with a streamlined but functionally deliberate corporate structure. The parent company is incorporated in Québec and headquartered in Montréal, with a wholly owned U.S. subsidiary serving as the primary vehicle for regulatory engagement and commercialization. This structure is typical for a Canada-based issuer with a U.S.-centric revenue opportunity.

Following FDA approval, Milestone now operates as a single-product specialty pharmaceutical company. Internal resources are concentrated on medical oversight, regulatory compliance, commercial execution, and financial management. This focus reduces overhead but embeds high single-product exposure.

Manufacturing remains asset-light, relying on third-party partners for production, packaging, and distribution. While this limits capital intensity, it places a premium on vendor oversight and quality systems integration. Importantly, FDA approval implies that manufacturing processes and controls met regulatory standards at the time of approval, materially reducing pre-approval uncertainty, though execution and scale-up risk remains.

As a single-product company with outsourced manufacturing, Milestone remains sensitive to supply-chain disruptions and operational missteps. Governance and execution responsibility are therefore concentrated within a relatively small leadership team. This structure enables speed and alignment but increases key-person and process-maturity risk during early commercialization.

In sum, Milestone’s corporate structure is appropriate for a focused specialty pharmaceutical launch. It prioritizes efficiency and capital discipline while accepting higher sensitivity to execution quality, supply reliability, and leadership effectiveness.

CARDAMYST™ (etripamil)

Product Overview and Clinical Context

CARDAMYST™ is a prescription intranasal formulation of etripamil, a short-acting calcium channel blocker approved by the U.S. Food and Drug Administration in December 2025 for the conversion of acute symptomatic episodes of Paroxysmal Supraventricular Tachycardia (PSVT) to sinus rhythm in adults.

The approval represents a meaningful inflection in the PSVT treatment landscape. It is the first FDA-approved therapy for PSVT in more than three decades and the first specifically designed for patient self-administration outside a supervised healthcare setting.

PSVT is characterized by sudden, episodic onset of rapid heart rhythms, most commonly mediated through the atrioventricular (AV) node. While not typically life-threatening, episodes are often highly symptomatic, unpredictable, and disruptive. Patients frequently experience severe palpitations, dyspnea, chest discomfort, dizziness, and anxiety. Because effective acute therapies have historically required intravenous administration under medical supervision, many patients default to emergency department visits or urgent care when episodes do not terminate spontaneously or with vagal maneuvers. This dynamic has imposed significant emotional burden on patients and driven substantial healthcare resource utilization.

CARDAMYST directly addresses this structural inefficiency by enabling treatment at symptom onset rather than after escalation to emergency care. By delivering a rapid-acting calcium channel blocker intranasally, the product allows timely intervention in home or community settings. Its value proposition therefore extends beyond rhythm conversion to include reduced episode duration, improved quality of life, greater patient autonomy, and lower system-level costs associated with avoidable emergency care.

FDA approval was supported by a comprehensive clinical program encompassing safety data from more than 1,800 participants and over 2,000 treated PSVT episodes. The program was anchored by the pivotal Phase 3 RAPID trial, a global, randomized, double-blind, placebo-controlled study evaluating self-administered etripamil in an unsupervised setting. RAPID demonstrated a statistically robust and clinically meaningful increase in rapid conversion to sinus rhythm versus placebo, with results published in The Lancet. These data formed the core of the regulatory submission and validated the real-world feasibility of unsupervised use.

CARDAMYST therefore enters the market not as an incremental reformulation, but as a purpose-built therapy designed to relocate acute PSVT treatment from the hospital to the patient. Its approval reflects both clinical efficacy and regulatory acceptance of self-administered cardiovascular therapies when supported by appropriate pharmacology, safety margins, and patient education.

Mechanism of Action and Pharmacologic Rationale

Etripamil is a short-acting L-type calcium channel inhibitor that exerts its primary pharmacologic effect at the atrioventricular node. By inhibiting calcium influx into AV nodal cells, etripamil slows conduction and increases refractoriness within the node, interrupting the re-entrant circuits responsible for the majority of PSVT episodes. Because over 90% of PSVT cases are AV-nodal dependent, this mechanism directly targets the dominant pathophysiology of the condition.

The mechanism is well established and familiar to cardiologists. Intravenous calcium channel blockers such as verapamil and diltiazem have been used for decades in emergency and inpatient settings to terminate PSVT via the same electrophysiologic pathway. CARDAMYST does not introduce a novel biologic concept; it adapts a trusted mechanism into a formulation optimized for rapid, on-demand use outside the hospital.

What differentiates etripamil is its pharmacokinetic profile and route of administration. Intranasal delivery enables rapid systemic absorption via the nasal mucosa, bypassing gastrointestinal absorption and first-pass metabolism. Following a single 70 mg dose, median time to peak plasma concentration is approximately seven minutes. This rapid onset aligns closely with clinical need, where prompt symptom relief is paramount.

Pharmacodynamically, etripamil produces a prompt but controlled effect on AV nodal conduction, prolonging the PR interval by approximately 8–10% within minutes of dosing. Importantly, this effect diminishes rapidly as plasma concentrations decline. Average concentrations fall by roughly 60% within 25 minutes of peak and by 80% within 60 minutes, with a terminal half-life of approximately 2.5 hours. Even at supratherapeutic exposure, etripamil does not meaningfully prolong the QTc interval.

This rapid on-off profile is deliberate. It allows effective termination of PSVT while minimizing prolonged hypotension, bradycardia, or high-grade AV block. The balance between potency and reversibility is central to CARDAMYST’s suitability for unsupervised, patient-administered use.

Clinical Efficacy and Safety Profile

Clinical efficacy is anchored by the RAPID Phase 3 trial. In the primary efficacy population with adjudicated PSVT, 64% of patients treated with CARDAMYST converted to sinus rhythm within 30 minutes, compared with 31% in the placebo arm. This corresponded to a hazard ratio of approximately 2.6 (P < 0.001), demonstrating a strong and clinically meaningful treatment effect.

Speed of action is critical in PSVT. Median time to conversion was 17.2 minutes with CARDAMYST versus 53.5 minutes with placebo. This difference is highly relevant in real-world settings, where prolonged symptoms frequently precipitate emergency care. The benefit persisted beyond the initial 30-minute window, reinforcing durability once conversion occurred.

Efficacy was consistent across key subgroups, including age, sex, geography, and background use of beta blockers or oral calcium channel blockers. Approximately two-thirds of patients were on background rate-controlling therapy, supporting CARDAMYST’s use as an episodic intervention layered on top of chronic management.

The safety profile reflects both the pharmacology of a short-acting calcium channel blocker and the intranasal route. Most adverse events were local and mild to moderate, including nasal discomfort, congestion, rhinorrhea, throat irritation, and epistaxis. Systemic cardiovascular events were uncommon. Clinically significant hypotension during test dosing occurred in approximately 0.4 percent of patients, and syncope within 24 hours occurred in approximately 0.1 percent. No cases of high-grade AV block or clinically meaningful QT prolongation were observed.

Overall, the benefit–risk profile supports CARDAMYST’s intended role as an at-home, on-demand therapy for appropriately selected patients.

Dosing, Use, and Practical Design

CARDAMYST is supplied as a disposable, single-use intranasal spray device. Each device delivers a total dose of 70 mg, administered as one spray into each nostril at symptom onset. If symptoms persist after 10 minutes, a second 70 mg dose may be administered using a new device. The maximum recommended dose is 140 mg within 24 hours.

Patients are instructed to seek medical care if symptoms persist 20 minutes after the second dose. Administration is advised in a seated position to mitigate fall risk associated with transient hypotension or dizziness.

The device requires no priming or assembly and is discarded after use, minimizing user error during acute symptomatic episodes. Portability is central to the design, allowing patients to initiate treatment wherever an episode occurs. This operational simplicity is critical given the anxiety and impaired concentration that often accompany PSVT.

FDA Label Overview

CARDAMYST is approved for acute conversion of PSVT in adults only. The label explicitly permits patient self-administration and repeat dosing within a single episode, while clearly defining contraindications, including moderate to severe heart failure, pre-excitation syndromes, and high-grade AV block without pacing.

The primary warning relates to hemodynamic effects such as hypotension or syncope. Adverse reactions are predominantly local and transient. The label provides a solid regulatory foundation for payer engagement while maintaining narrow, defensible boundaries around approved use.

Strategic Importance and Forward Optionality

PSVT approval establishes etripamil as a marketed cardiovascular therapy with validated safety, manufacturing, and real-world use precedent. This materially de-risks future label expansion, most notably atrial fibrillation with rapid ventricular rate (AFib-RVR), which Milestone intends to pursue via a supplemental NDA.

A positive Phase 2 AFib-RVR study (ReVeRA) supports this extension, and FDA guidance indicates that a single pivotal Phase 3 trial could support approval. However, management has deliberately avoided embedding AFib-RVR upside into near-term commercial narratives. This restraint is appropriate. PSVT execution remains the core value driver, with AFib-RVR treated as additive optionality rather than a base-case assumption.

Section Summary

CARDAMYST combines a well-understood pharmacologic mechanism with a delivery profile specifically engineered for acute, unsupervised use. Its approval represents a structural shift in PSVT care, enabling patients to intervene early rather than escalate to emergency settings.

At this stage, success is no longer defined by science or regulatory outcomes. It is defined by execution: prescriber adoption, payer alignment, patient education, and supply reliability. If Milestone executes effectively, CARDAMYST has the potential to become the default acute intervention for PSVT, representing not just commercial success, but a durable change in clinical practice.

Strategic Concentration and the Deliberate Lack of Pipeline Optionality

Milestone Pharmaceuticals is best understood by what it has intentionally chosen not to be. The company does not operate a discovery platform, does not maintain a broad preclinical engine, and has not built a diversified early-stage clinical pipeline. It has not disclosed multiple parallel programs, exploratory cardiovascular franchises, or non-cardiovascular expansion efforts. Its disclosed development focus remains narrow: etripamil as CARDAMYST in PSVT, and the potential label expansion into atrial fibrillation with rapid ventricular rate.

This absence of pipeline breadth is not a temporary gap or a transitional phase. It reflects a deliberate strategic posture. Management has consistently prioritized focus, capital discipline, and execution certainty over optionality. Rather than spreading limited organizational capacity across multiple “shots on goal”, Milestone concentrated resources on taking one product from late-stage development through regulatory approval and into commercialization. That choice reduces scientific and operational complexity, but it also removes the diversification buffer that many biotech and specialty pharma companies rely on to absorb setbacks.

The consequence is structural. Milestone’s value creation remains tightly coupled to CARDAMYST. There is no second asset capable of independently generating value if the launch underperforms. There is no platform that can be repurposed, licensed, or monetized to create an alternative narrative. AFib-RVR is credible and potentially meaningful, but it remains an extension of the same molecule, delivery system, and core pharmacology. Until a label expansion is approved and commercially relevant, it does not materially reduce concentration risk.

This structure raises the bar for execution. With no alternate revenue stream or pipeline catalyst to soften volatility, early launch performance in PSVT will disproportionately shape investor perception, capital access, and strategic flexibility. Under this model, adoption, payer coverage, and supply reliability are not just contributors to success; they are the success. Any meaningful misstep in any of these areas has immediate implications because there is no internal portfolio to stabilize results.

At the same time, the narrow strategy offers clarity that many biopharma companies lack. Management attention is not diluted, incentives are aligned around one objective, and capital allocation becomes straightforward. For investors, the proposition is transparent. Milestone will be rewarded if it can establish CARDAMYST as a durable, routine acute therapy for PSVT and only then leverage that foundation into adjacent indications.

In sum, Milestone’s lack of pipeline optionality is both a constraint and a defining feature of its identity. It magnifies downside if execution falls short, but it also reflects a company built to do one thing well. AFib-RVR can broaden the value base over time, but until then, Milestone remains a focused single-asset operator whose outcomes are inseparable from the commercial success of CARDAMYST.

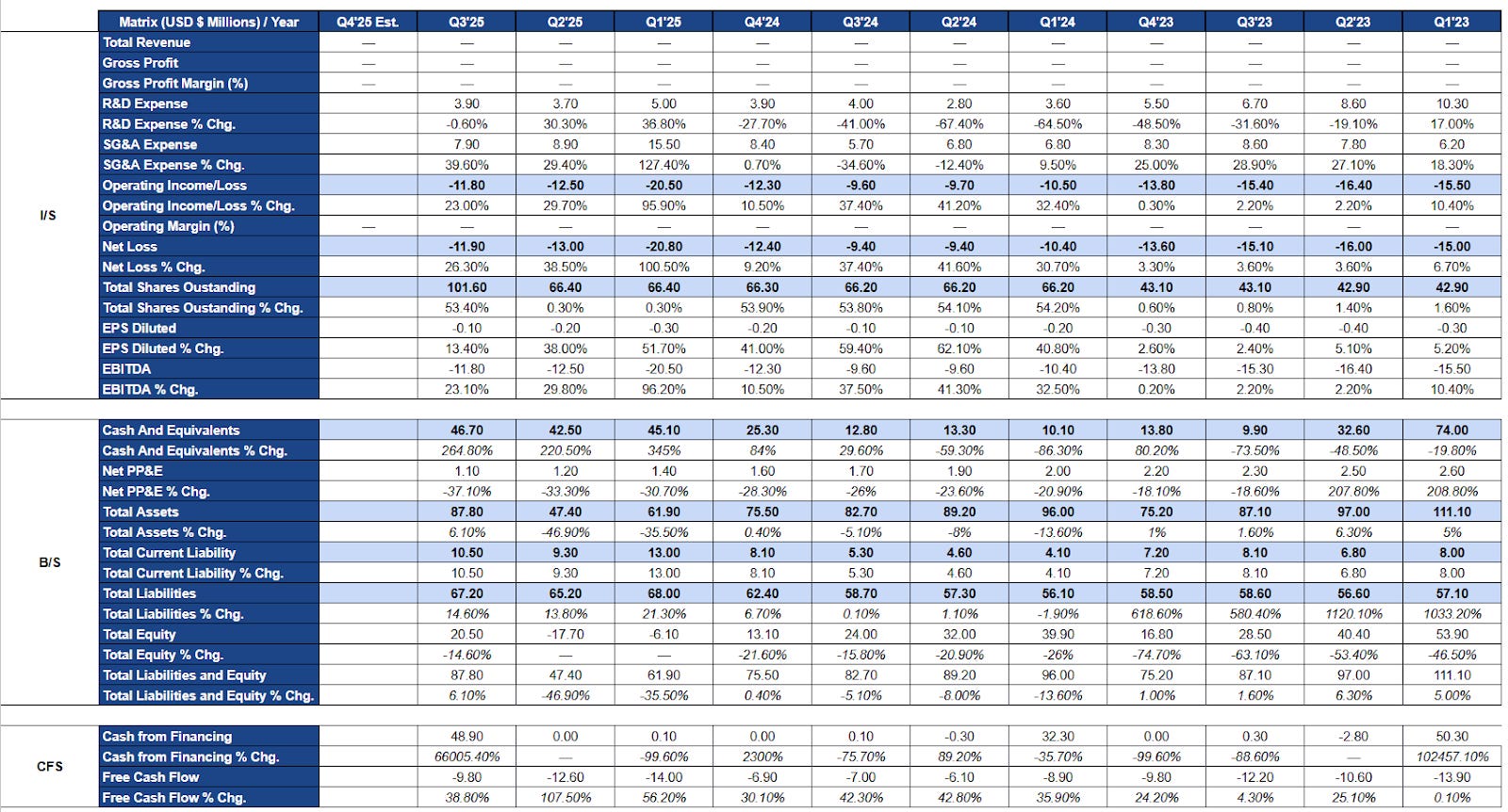

Financial Analysis (2023–Q3 2025)

Milestone Pharmaceuticals’ financial statements from 2023 through the third quarter of 2025 reflect a company executing a controlled transition from late-stage clinical development into pre-commercial readiness. The absence of revenue throughout this period is neither anomalous nor concerning. It is a structural feature of the business prior to FDA approval of CARDAMYST. Management did not attempt to accelerate revenue recognition or pursue marginal pre-launch monetization strategies, leaving the income statement clean and analytically transparent.

As a result, financial evaluation during this period is best framed around cost structure evolution, cash discipline, and balance sheet management rather than profitability. On these dimensions, the financials show a coherent and intentional pattern aligned with the company’s strategic progression.

Income Statement Analysis

Research and development expenses exhibit a sustained structural decline rather than cyclical volatility. In early 2023, quarterly R&D spending exceeded ten million dollars, reflecting the intensity of late-stage clinical trials, regulatory submission activities, and manufacturing readiness for the PSVT program. As these milestones were completed, R&D spend normalized into the three to five million dollar range by 2024 and remained at comparable levels through 2025.

This decline is consistent with the conclusion of pivotal Phase 3 work and the absence of a discovery platform or parallel development programs. Importantly, R&D spending did not collapse. Residual investment supports post-approval pharmacovigilance, regulatory commitments, medical oversight, and preparatory work related to a potential AFib-RVR expansion. This reflects disciplined maintenance of scientific and regulatory obligations rather than disengagement from clinical rigor.

In contrast, selling, general, and administrative expenses show a clear inflection beginning in late 2024 and accelerating into 2025. This marks Milestone’s transition from a development-focused organization to a commercial-stage operator. SG&A growth aligns with the build-out of commercial infrastructure, including sales force hiring, market access and payer contracting, medical affairs expansion, distribution planning, and patient support initiatives.

While SG&A growth rates appear elevated on a year-over-year basis, they are best interpreted in the context of a low starting base rather than uncontrolled expansion. Critically, increased SG&A has been largely offset by the systematic reduction in R&D spending, resulting in total operating expenses that remain relatively stable and predictable.

This cost reallocation is reflected in operating income and net loss trends. Despite a meaningful shift in expense composition, quarterly operating losses remain contained within a consistent range, generally in the high single-digit to low double-digit millions. There is no evidence of operating leverage working against the company, nor signs of cost slippage during commercialization preparation. The modest widening of losses in early 2025 aligns with front-loaded launch costs and financing-related items rather than deterioration in operating discipline.

Earnings per share trends reinforce this interpretation. Share count increases through 2024 and into 2025 reflect episodic equity financing undertaken to secure runway ahead of approval and launch. Dilution appears milestone-driven rather than continuous, suggesting proactive capital raising rather than reactive financing under stress. Notably, net losses did not accelerate in proportion to dilution, indicating that capital was used to stabilize the balance sheet rather than fund uncontrolled expansion.

Overall, the income statement reflects a controlled transition. Peak development spending was wound down, capital was redeployed into commercial readiness, and operating losses were kept stable throughout. The income statement has moved away from binary development risk and now reflects early-stage execution risk.

Balance Sheet Analysis

Milestone’s balance sheet provides a clear view of liquidity management during its transition into pre-commercial operations. Cash balances exhibit quarter-to-quarter variability, but this volatility is intentional and explainable. Cash declines align with periods of elevated operating spend, while sharp increases correspond to discrete financing events rather than unexplained inflows.

This pattern indicates active runway management. Financing was structured around known inflection points rather than short-term liquidity pressure. By the third quarter of 2025, Milestone entered the regulatory approval window with a reinforced cash position, reflecting deliberate pre-launch planning rather than last-minute balance sheet repair.

Total assets decline gradually over time, which is appropriate for a company consuming cash to fund operations without capitalizing development costs or manufacturing infrastructure. Management avoided aggressive capitalization of R&D, intangibles, or pre-commercial inventory, resulting in a balance sheet that reflects economic reality rather than accounting optics.

Liabilities remain modest and stable. There is no evidence of leverage being used to fund operations, nor signs of stress in payables or accruals. The absence of debt materially reduces financial risk and preserves flexibility as the company transitions toward revenue generation.

Equity movements are driven by cumulative operating losses offset by episodic capital raises. Dilution was applied strategically to support milestones rather than cover unforeseen shortfalls. This proportional and well-timed approach distinguishes Milestone from peers that rely on serial financing to manage uncontrolled burn.

Taken together, the balance sheet reflects liquidity discipline, transparency, and structural simplicity. For a single-asset company entering commercialization, this clarity is a material strength.

Cash Flow Statement Analysis

Cash flow statements provide the clearest validation of Milestone’s financial discipline. From 2023 through Q3 2025, free cash flow remains consistently negative, as expected for a pre-revenue company. What stands out is not the existence of burn, but its predictability. Quarterly cash outflows remain within a relatively narrow range despite a substantial internal shift in spending priorities.

As commercialization expenses increased, there was no corresponding acceleration in cash burn. This reflects a substitution of spending rather than cost layering. R&D spend declined as SG&A rose, preventing the overlapping cost structures that often destabilize companies during launch preparation.

Operating cash outflows dominate free cash flow, while capital expenditures remain minimal and stable. This is consistent with Milestone’s asset-light model and reliance on third-party manufacturing. The absence of irregular capital spending further reduces liquidity shock risk.

Financing inflows are episodic and milestone-linked. Capital raises align with regulatory and strategic events rather than ongoing operational deficits. This approach reduces cumulative dilution and indicates capital planning rather than urgency.

Overall, cash flow data confirm that Milestone imposed financial discipline before entering commercialization. Spending has been aligned with strategy, and funding has been secured deliberately rather than defensively.

Financial Health, Solvency, and Execution Readiness

Entering commercialization, Milestone’s financial health is best described as stable but highly concentrated. The company remains pre-revenue, but it has eliminated many of the structural weaknesses that derail late-stage transitions. There is no evidence of uncontrolled cost growth, liquidity mismanagement, or balance sheet leverage that would impair near-term execution.

Liquidity adequacy is the central consideration at this stage. Based on historical burn rates and reported cash balances, Milestone appears to have sufficient runway to support early commercialization without immediate reliance on distressed financing. This provides management with the flexibility to prioritize execution quality over short-term capital preservation.

Solvency risk is low. The balance sheet carries no meaningful debt, and liabilities are modest. This simplicity allows future gross profit, when generated, to flow into operating leverage rather than debt service or structural obligations.

That said, financial resilience is inseparable from concentration risk. Milestone is a single-asset company with no diversified revenue base or pipeline monetization to offset commercial underperformance. As a result, the company’s financial durability depends almost entirely on converting commercial spend into sustained adoption.

The mitigating factor is capital discipline. SG&A has been scaled gradually rather than aggressively, preserving flexibility. If early launch metrics underperform, spending can be moderated without destabilizing operations. If uptake is strong, the balance sheet can support incremental investment to accelerate growth.

From an execution standpoint, the financials suggest that most structural transition costs have already been absorbed. Management is positioned to focus on pricing, payer access, field execution, and patient education rather than financial triage.

In summary, Milestone’s financial health is defined less by absolute strength than by preparedness. The framework is coherent, disciplined, and aligned with a single execution-driven launch. The remaining risk is commercial, not financial. If CARDAMYST adoption meets even modest expectations, the existing structure can support a path toward operating leverage. If adoption disappoints, concentration risk will dominate. The financial statements make this trade-off explicit and provide a clear lens through which to evaluate the company’s next phase.

Valuation Analysis

Valuation Framework and Methodology

Milestone Pharmaceuticals should be valued using a risk-adjusted, scenario-based framework anchored to commercialization outcomes, not traditional multiples or near-term earnings optics. The company has no revenue history through the analyzed periods, continues to report operating losses, and remains economically dependent on a single commercial asset. Under these conditions, conventional tools such as EV/EBITDA, P/E, or even forward revenue multiples can create the illusion of precision while masking the true drivers of value. They implicitly assume a stable economic profile that Milestone has not yet earned.

The appropriate methodology is a risk-adjusted net present value framework that models distinct adoption paths for CARDAMYST in PSVT and treats AFib-RVR as separately probability-weighted upside. This structure aligns valuation with the business’s real economic engine. Value will be determined by prescription uptake, repeat utilization, payer access, and operating leverage. An rNPV framework forces those drivers into explicit assumptions rather than letting them hide inside a single blended “forecast”.

This is not a traditional pre-approval pipeline rNPV. In Milestone’s case, PSVT approval has largely removed binary regulatory uncertainty. The remaining risks are continuous and execution-driven. Access friction, prescribing inertia, patient education, distribution reliability, and real-world use patterns are not well captured by a single-point forecast or a generic probability-of-success adjustment. Discrete scenario analysis is therefore required to represent the range of plausible commercial realities.

Structuring valuation around coherent scenarios rather than a single blended case improves analytical honesty. It makes assumptions transparent, limits model fragility, and avoids long-dated terminal value dependence. At this stage, the goal is not micro-precision. The goal is to map outcomes to the handful of variables that will actually determine shareholder returns.

Core Valuation Assumptions

The valuation is intentionally built on a narrow set of high-impact assumptions to reduce fragility. In a single-asset early launch, small changes in a handful of variables dominate results. The objective is realism and stress-testability, not maximal upside.

The addressable market is defined conservatively as adults with recurrent PSVT who are clinically appropriate and behaviorally likely to use an on-demand, self-administered therapy. This excludes the full prevalence pool. Many patients experience infrequent episodes, are controlled on chronic regimens, or will not be prescribed a rescue therapy. It also excludes populations where self-administration is clinically unsuitable. Penetration is modeled as gradual, reflecting both cardiology’s conservative adoption curve and the time required for payer pathways and physician habits to normalize.

Pricing assumptions are anchored to CARDAMYST’s practical economic role rather than theoretical willingness to pay. The drug is positioned as an episodic specialty cardiovascular intervention with a system-level cost-offset narrative, but it is not a chronic daily therapy. Net pricing is modeled conservatively with meaningful gross-to-net adjustments for rebates, patient support, distribution economics, and payer controls. No meaningful price escalation is assumed, and the model does not depend on list-price expansion to drive value.

Cost structure assumptions follow observed behavior rather than aspirational margins. SG&A remains elevated through early commercialization as Milestone invests in field execution, market access, medical affairs, and patient support. Operating leverage is not assumed immediately. SG&A efficiency improves only as volumes scale and fixed commercial infrastructure is absorbed over a larger revenue base. R&D remains modest but persistent, reflecting post-marketing obligations, lifecycle work, and AFib-RVR development.

The discount rate is set in the low-to-mid teens to reflect single-asset concentration, small-cap liquidity risk, and early commercial execution uncertainty. Regulatory risk has been reduced for PSVT, but the remaining risks are operational and behavioral, warranting a higher discount rate than mature, diversified specialty pharma peers.

Terminal value reliance is deliberately restrained. The model places the majority of value creation within the first eight to ten years post-launch, when adoption dynamics and margin expansion are most observable. This reduces sensitivity to long-dated assumptions and reflects the reality that durability depends on factors that are not forecastable today.

These assumptions prioritize robustness over optimism. They reflect a view that Milestone’s value will be driven by execution quality and adoption dynamics, not pricing leverage or speculative terminal growth.

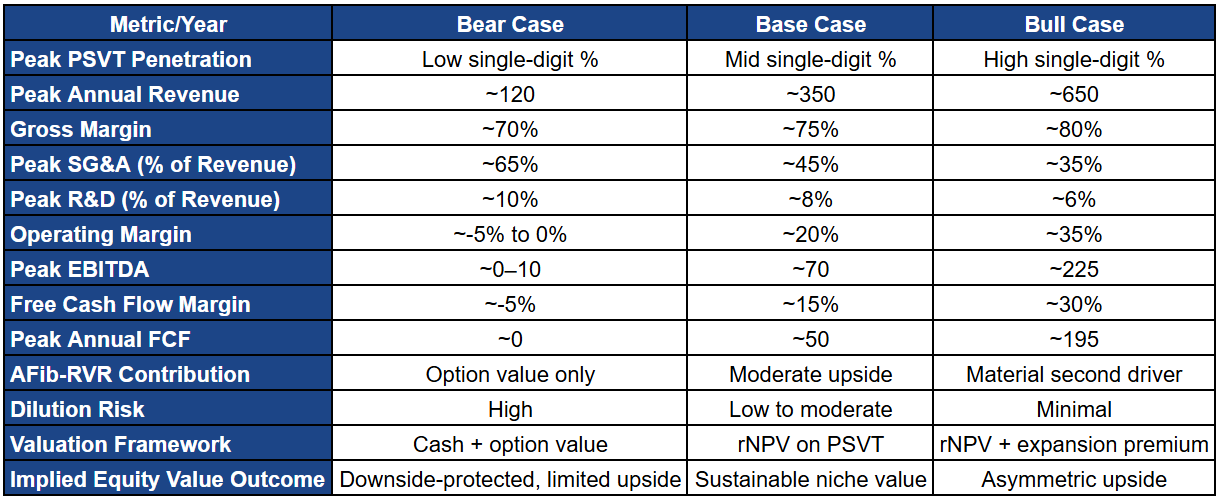

Scenario Analysis: Bear, Base, and Bull Cases

Milestone’s valuation is best framed through discrete commercialization scenarios. With scientific and regulatory questions largely resolved for PSVT, shareholder outcomes are now dominated by execution: adoption velocity, payer normalization, repeat utilization, and operating leverage. Each scenario represents a coherent commercial reality that could plausibly emerge during the first five to seven years after launch.

Bear Case: Limited Adoption, Delayed Economics, Valuation Anchored to Optionality

In the bear case, adoption remains constrained by physician inertia and persistent access friction. Uptake concentrates within a narrow cohort of electrophysiologists and high-conviction cardiologists, while broader community cardiology adoption fails to scale. This is not clinical failure. It is slow behavior change, conservatism around unsupervised use, and insufficient urgency to modify established care pathways.

Payers add friction rather than momentum. Prior authorization, step therapy, and inconsistent coverage suppress utilization and repeat behavior. Even where the emergency department avoidance logic is acknowledged, it does not translate into streamlined access. Patients face delays and administrative burden that weaken persistence and normalize CARDAMYST as an “episodic rescue” rather than a routinely prescribed tool.

Commercially, treated patient counts ramp slowly. About 5,000 in year one grows to roughly 35,000 by year three and around 110,000 by year five, remaining below 20% penetration of the addressable PSVT pool. Net revenue rises from low single-digit millions in year one to roughly $100+ million by year five, driven primarily by incremental patient adds rather than strong repeat usage or improved access.

Financially, this trajectory prevents meaningful operating leverage. Gross margins improve gradually, but the revenue base cannot absorb the fixed costs of commercial infrastructure. SG&A remains elevated because reducing it would impair already-fragile growth. EBITDA remains negative across the five-year horizon, free cash flow stays negative, and cumulative burn becomes material. External financing remains necessary, making dilution a persistent feature rather than a one-time bridge.

In valuation terms, this becomes a solvency-and-optionality story. The company survives because it is asset-light and disciplined, but it does not compound capital. Equity value is anchored to liquidity, residual PSVT option value, and the long-dated possibility of AFib-RVR rather than earnings power. The bear case illustrates the central truth of Milestone: CARDAMYST does not need to fail clinically for shareholder outcomes to disappoint. Modest execution friction is enough.

Base Case: Sustainable Niche Adoption and Mid-Cycle Profitability

In the base case, CARDAMYST performs as a successful niche cardiovascular therapy. Adoption grows steadily through cardiologists and electrophysiologists managing recurrent PSVT patients, especially those with prior ED utilization. Physician confidence builds through real-world familiarity rather than heavy promotion, consistent with cardiovascular adoption dynamics.

Payer coverage improves incrementally. ED avoidance becomes a practical economic argument over time, coverage normalizes, and administrative friction declines. Repeat utilization improves as both patients and physicians become comfortable with on-demand self-administration. Growth is driven by routine incorporation rather than one-off trial use.

Commercially, treated patients rise from roughly 10,000 in year one to about 80,000 by year three and exceed ~220,000 by year five, reaching roughly one-third penetration of the addressable pool. Net revenue scales from roughly $7.5 million in year one to above $200 million by year five, supported by improving access, better repeat utilization, and cleaner payer mix rather than aggressive pricing.

Financially, operating leverage emerges on a credible timetable. SG&A remains elevated early but begins to grow more slowly than revenue by year three. EBITDA losses narrow through years two and three, break-even occurs around year four, and by year five EBITDA becomes meaningfully positive with free cash flow firmly positive. This is the threshold that matters: once self-funding is achieved, the company’s dependence on external capital drops sharply and AFib-RVR becomes fundable rather than aspirational.

Valuation in the base case transitions from “cash plus optionality” to “durable specialty pharma economics”. Your valuation range is coherent: roughly $450 million at the low end, ~$600 million at the midpoint, and ~$750 million at the upper end, translating to approximately $4.25, $5.75, and $7.25 per share respectively (based on your diluted share count assumption). This outcome does not require blockbuster claims. It requires disciplined execution and steady adoption.

Bull Case: Rapid Adoption, Early Leverage, and Expansion Optionality

In the bull case, physician behavior shifts faster than expected and early real-world success accelerates confidence. CARDAMYST becomes integrated into standard PSVT pathways among electrophysiologists and cardiologists as a default acute option outside the ED. Patient self-administration proves reliable, reducing prescriber hesitation and increasing repeat behavior.

Payer alignment becomes an accelerant rather than a brake. Coverage reflects the ED avoidance logic early, administrative friction drops faster, and out-of-pocket barriers are manageable. This supports higher adherence and faster normalization of CARDAMYST as a routine prescription for recurrent PSVT.

Commercially, treated patients rise from roughly 15,000 in year one to ~140,000 by year three and exceed ~360,000 by year five, approaching ~60% penetration of the addressable pool. Net revenue exceeds $340 million by year five. Importantly, the bull case is still a specialist-driven franchise, not a primary-care phenomenon, and it does not require pricing aggression.

Financially, scale unlocks earlier leverage. SG&A grows slowly relative to revenue as fixed infrastructure is absorbed, EBITDA turns positive earlier than in the base case, and free cash flow accelerates. The capital structure changes meaningfully: self-funding arrives earlier, dilution risk collapses, and AFib-RVR becomes an internally financeable growth program rather than conditional upside.

Valuation in the bull case shifts toward EBITDA and growth-multiple logic. Your range is coherent: ~$900 million for a lower bull outcome, ~$1.2 billion at the midpoint, and up to ~$1.6 billion in an upper bull outcome, implying approximately $8.50, $11.25, and $15.00 per share respectively (again based on your diluted share assumption). This is execution upside, not science upside.

Risk-Adjusted Valuation and Probability Weighting

A credible valuation must probability-weight outcomes rather than anchor on a single scenario. With PSVT approval in hand, Milestone’s risk profile is execution-driven and asymmetric: downside is bounded by solvency and cost control, while upside depends on adoption speed and payer normalization.

The base case deserves the highest weight because it reflects a defensible commercialization path consistent with specialty cardiovascular launches. The bear case remains material because in a single-asset model, modest underperformance in adoption or access can impair value quickly. That said, catastrophic downside is mitigated by Milestone’s asset-light structure, controlled expense scaling, and lack of balance sheet leverage. The bull case is less probable but not speculative. It requires faster behavior change and earlier payer alignment, not new science.

AFib-RVR should be treated as explicit optionality layered on top of PSVT rather than embedded implicitly in terminal assumptions. This preserves risk boundaries and avoids overstating certainty.

Risk-Adjusted Equity Valuation: PSVT Core

Using your defined equity values and weights:

Bear: $230m, 25% probability → $58m probability-weighted

Base (midpoint): $600m, 50% probability → $300m probability-weighted

Bull (midpoint): $1,200m, 25% probability → $300m probability-weighted

This produces a risk-adjusted PSVT core equity value of approximately $658 million.

AFib-RVR Explicit Optionality

AFib-RVR should be valued separately and discounted for development and execution risk. Under your conservative treatment:

Unrisked upside: ~$300–$400m

Probability of success: ~30%

Discounted PV contribution: ~$100–$120m

Using your midpoint, AFib-RVR adds approximately $110 million.

Total Risk-Adjusted Equity Value

Combining PSVT core value (~$658m) with AFib-RVR optionality (~$110m) yields total risk-adjusted equity value of approximately $770 million.

Assuming a fully diluted share count of ~105–110 million, this supports a high single-digit per-share valuation, consistent with an outcome that sits between base and bull and matches the company’s current execution profile.

Valuation Bottom Line

Milestone’s valuation is no longer about whether CARDAMYST works. That has largely been resolved. The equity outcome now depends on whether commercial spending converts into sustained prescribing behavior and whether management can make CARDAMYST routine rather than episodic.

A scenario-weighted framework makes this explicit. Downside is bounded by cost discipline, an asset-light model, and solvency. Upside is determined by adoption velocity, payer normalization, and repeat utilization. The market will ultimately reward Milestone not for approval, but for evidence of scalable, repeatable commercial execution. In that environment, single-point targets create false precision. Scenario-weighted valuation is the cleaner tool.

Commercial Launch Guidance and Expectations from the Initial 60-Rep Sales Force

Milestone’s launch plan is deliberately restrained. A roughly 60-rep build is not meant to “win on volume” in year one. It is meant to prove that CARDAMYST can be prescribed predictably, reimbursed with manageable friction, and used repeatedly by the right patients. This is a behavior-change launch, not a demand-surge launch. If the model works at this scale, it can be scaled. If it fails at this scale, adding bodies only burns cash faster.

Targeting Strategy and Coverage Expectations

With CARDAMYST, the commercial target is not “all cardiology”. It is a curated prescriber universe that already sees recurrent PSVT and already deals with the downstream inefficiency of ED escalation. That typically means electrophysiologists and high-volume cardiologists who manage arrhythmia patients longitudinally, recognize PSVT quickly, and can identify appropriate candidates before the next episode occurs. These clinicians disproportionately shape local practice norms, and they are the most likely to generate repeat usage because they have the highest density of the right patients.

A 60-rep field team implies disciplined coverage rather than broad reach. In practice, each rep can manage something like 150 to 200 priority accounts, which maps to an initial universe of roughly 9,000 to 12,000 physicians. That aligns with management’s stated targeting logic and fits the reality that PSVT prescribing is naturally concentrated. The operational implication is important: Milestone does not need to blanket the country to create meaningful early signals. It needs depth in the right offices, consistent follow-up, and reliable conversion from “interest” to “routine prescribing”.

Early Launch Metrics That Matter

Investors should not judge the first few quarters by absolute revenue. Early revenue is a lagging indicator and can look deceptively weak even if the launch is working, because the product is episodic and because payer pathways take time to normalize. What matters early is whether CARDAMYST is embedding into workflow, and that shows up in leading indicators.

The most important leading indicators are prescribing breadth across the target list, repeat prescribing within early adopters, and patient-level persistence signals (repeat fills and repeat episode use where appropriate). A healthy launch is not just “more prescribers”. It is higher density in the prescribers that matter, meaning physicians who try it and then keep using it, because they see reliable conversion, patients can self-administer correctly, and access barriers are not constantly breaking the process. If scripts are high but repeat behavior is weak, that is promotional trialing, not adoption.

Qualitative feedback also matters more than most investors admit. Early comments from cardiologists and EPs about patient selection, ease of use during an episode, tolerability, and the practicality of the refill process will often predict the shape of year two better than any single quarter of script data.

Payer and Access Coordination

In this launch, market access is not “supporting” sales. It is a primary determinant of whether sales effort converts into durable utilization. Even a motivated prescriber will stop using the product if prior authorization is inconsistent, if the pharmacy process is unreliable, or if patient out-of-pocket costs create abandonment.

The sales force’s job here is partly commercial and partly diagnostic. Reps will be the first to see where the system breaks: which plans block coverage, where step therapy shows up, which specialty pharmacy workflows create delays, and how frequently prescriptions die between writing and dispensing. That field feedback loop becomes operational intelligence for the market access team, allowing Milestone to refine payer strategy, fix friction points, and prioritize contracting efforts that actually move persistence.

The core launch risk is not “do doctors like it”. It is “can doctors repeatedly get it for patients without an administrative nightmare”. The initial field footprint must surface that truth quickly.

Realistic Expectations for Year One Performance

With 60 reps, Milestone should not be expected to generate immediate scale economics, and management is not trying to. Year one is a controlled ramp designed to validate repeatable demand creation and identify the most productive prescriber segments. The right way to frame year one is as the phase where Milestone proves that CARDAMYST can transition from an interesting concept into a repeatable prescribing habit inside a targeted specialist footprint.

If the launch is executing well, year one should produce three outcomes. First, a defined base of prescribers who have moved beyond one-time trialing and are writing repeat scripts. Second, a growing cohort of patients who can obtain and use the product correctly and who remain on therapy when episodes recur. Third, a clear map of where commercialization dollars generate the highest return, which informs whether sales force expansion is rational or premature.

Bottom Line on the Initial Sales Deployment

The initial 60-rep build is a calibration instrument. Its purpose is to generate high-quality signals: does adoption concentrate and deepen, do access barriers normalize, and does repeat usage emerge in the right patients. If Milestone can show that a modest, well-targeted team can drive repeat prescribing and payer traction, it validates the scalability of the model and supports rational expansion.

If density does not emerge inside this focused footprint, expanding the sales force will not fix the problem. It will only amplify cost. In that case, the issue is almost always structural, meaning access friction, workflow mismatch, or weak persistence, not “not enough reps”. The first year is therefore less about ambition and more about proof.

Payer Economics: Medicare, Medicaid, and Commercial Insurance Dynamics

Payer behavior will be one of the decisive variables in CARDAMYST’s commercial outcome. This is not a drug whose value is realized through long-term adherence curves or chronic disease modification. It is an acute, episodic intervention whose economics are built on cost avoidance, specifically the displacement of emergency department utilization. That places CARDAMYST in a gray zone between the pharmacy benefit and the medical benefit, where incentives differ materially across Medicare, Medicaid, and commercial plans. How quickly those incentives align will matter as much as physician willingness to prescribe.

Medicare: Cost Avoidance Is the Core Lever

Medicare is likely to represent a meaningful share of CARDAMYST’s mature payer mix given the age distribution of recurrent PSVT patients. Structurally, Medicare’s incentives are well aligned with the product’s value proposition. Emergency department visits for PSVT are expensive, often trigger additional diagnostic workups, and contribute to rising episode-of-care costs that Medicare Advantage plans in particular are incentivized to suppress.

For Medicare Advantage, CARDAMYST fits cleanly into a total-cost-of-care framework. A self-administered therapy that reliably terminates PSVT outside the hospital directly reduces ED claims and downstream spend. Once real-world data demonstrate that effect, coverage logic becomes straightforward. Traditional fee-for-service Medicare is slower to adapt, but coverage pathways tend to stabilize once coding, formulary status, and medical necessity criteria are clearly defined.

Early friction should be expected. Prior authorization and utilization controls will likely be applied initially to enforce appropriate patient selection. Over time, however, Medicare coverage should normalize as prescriber behavior solidifies and outcomes data accumulate. Medicare is therefore best viewed as a medium-term structural tailwind, not an immediate launch accelerator.

Medicaid: Access With Constrained Economics

Medicaid presents a very different economic profile. PSVT patients in Medicaid populations often exhibit higher emergency department utilization, which strengthens the theoretical cost-offset argument. In practice, however, Medicaid programs are extremely price-sensitive and heterogeneous across states in terms of formulary design, utilization controls, and reimbursement timelines.

CARDAMYST is likely to achieve broad Medicaid coverage over time, but net pricing will be meaningfully lower due to mandatory rebates and supplemental discounts. As a result, Medicaid contributes access and volume rather than margin. For Milestone, Medicaid should be viewed as strategically important but economically limited. It reinforces the public-health and cost-avoidance narrative, but it will not drive profitability.

Commercial Insurance: The Near-Term Battleground

Commercial payers will be the most important determinant of early commercial success. These plans face direct pressure from employers to control emergency department utilization and episodic acute-care spend, making them receptive to therapies that can shift care out of high-cost settings. At the same time, commercial coverage behavior is highly variable, especially for novel use cases.

For CARDAMYST, commercial insurers represent both the largest opportunity and the most immediate source of uncertainty. Some plans are likely to move quickly toward formulary inclusion based on the ED avoidance thesis. Others will initially impose prior authorization, step edits, or documentation requirements tied to recurrent PSVT episodes. Over time, plans that observe lower emergency department claims among CARDAMYST users should rationally reduce friction, improving repeat utilization and prescription velocity.

This channel is also where employer-sponsored plans and pharmacy benefit managers exert significant influence. Milestone’s ability to generate and communicate real-world economic evidence, including claims-based analyses and post-launch outcomes data, will materially affect how fast commercial coverage normalizes. In practice, payer engagement and evidence generation will be just as important as physician education in the first year.

Gross-to-Net Dynamics and Revenue Quality

Across all payer types, gross-to-net adjustments will be meaningful in the early commercialization phase. Rebates, patient assistance programs, and distribution fees will suppress net realized pricing as Milestone prioritizes access and utilization over margin optimization. This is normal for specialty cardiovascular launches and should not be misinterpreted as weak pricing power.

What matters more than list price is revenue quality. A smaller population of well-covered patients who refill and reuse the product appropriately will be far more valuable than broad but fragile access. As payer confidence improves and coverage stabilizes, gross-to-net dynamics should normalize, supporting margin expansion in later years.

Strategic Implications for Milestone

Payer economics reinforce the central execution thesis. CARDAMYST does not need universal coverage on day one, but it does need a credible path toward normalization in Medicare Advantage and commercial plans. The early commercial period should therefore be understood as a payer education and evidence-building phase, not a monetization sprint.

If Milestone can demonstrate that CARDAMYST reliably reduces emergency department utilization without creating offsetting downstream costs, payer alignment should follow. If access remains fragmented despite physician enthusiasm, adoption velocity will stall regardless of sales execution.

In short, payer dynamics are not peripheral to CARDAMYST’s story. Medicare provides structural support, Medicaid offers access with limited margin, and commercial insurers represent the decisive near-term lever. How effectively Milestone navigates these relationships will determine whether clinical validation translates into durable economic value.

Worldwide CARDAMYST Franchise: Intellectual Property and Competitive Moat

Ownership and Control of the Asset

Milestone retains full ownership of CARDAMYST and the underlying etripamil asset, with no structural encumbrances that would impair strategic flexibility or long-term economics. The company’s disclosures do not reveal layered royalty obligations, profit-sharing structures, or change-of-control provisions that would function as a de facto poison pill. This matters. From both an execution and M&A perspective, CARDAMYST is a clean asset that can be scaled, partnered, or acquired without the friction that often erodes value in small-cap specialty pharma.

The only meaningful geographic carve-out is Greater China, where rights have been licensed to Corxel Pharmaceuticals (formerly Ji Xing). This arrangement provides non-dilutive milestone payments and potential royalties while transferring development and commercialization responsibility in a complex regulatory and reimbursement environment to a local operator. While this limits absolute global upside, it is a rational trade-off. China carries high execution risk for foreign specialty pharma companies, and monetizing the region via a partner allows Milestone to concentrate capital and management attention on the U.S. and other ex-China markets where returns on effort are clearer. At Milestone’s current scale, this improves capital efficiency and reduces operational distraction, which is a net positive despite the capped upside.

Patent Life and Duration of Exclusivity

CARDAMYST’s intellectual property estate is appropriately constructed for a specialty pharmaceutical franchise. Core patents extend through approximately 2042, providing roughly 15 to 17 years of remaining protection from the start of commercialization. This duration is well within acceptable norms for pharmaceutical assets and supports long-term value creation without requiring aggressive near-term lifecycle maneuvers.

Importantly, Milestone has continued to strengthen its IP position beyond the initial approval. A recently issued U.S. patent covers the repeat-dose regimen, specifically the ability for patients to administer a second intranasal spray if the first dose does not terminate the PSVT episode. This protection is strategically significant. Repeat dosing is central to real-world usability, physician confidence, and patient adherence. By securing IP around this behaviorally critical feature, Milestone materially raises the barrier for generic competition.

The relevance of this dosing-related IP extends beyond the PSVT label. The same repeat-dose framework is expected to apply to future indications such as atrial fibrillation with rapid ventricular rate. As a result, the patent estate protects not only the current indication, but also anticipated lifecycle extensions, reinforcing the view of CARDAMYST as a franchise asset rather than a single-use product.

Longevity and Generic Risk Assessment

With patent protection extending into the early 2040s and no obvious near-term vulnerabilities, generic entry appears distant. Even as patent expiry approaches, erosion is likely to be slower than for conventional oral small molecules. The combination of a drug-device product, intranasal delivery, dosing-specific IP, and entrenched prescribing behavior creates additional friction for generic substitution and delays rapid commoditization.

From a valuation standpoint, the IP profile is sufficient to support both the base and bull case scenarios without relying on optimistic assumptions about perpetual exclusivity. It provides a clear and credible window for Milestone to scale the CARDAMYST franchise, achieve operating leverage, and potentially pursue strategic alternatives well before exclusivity becomes a constraining factor.

In short, CARDAMYST’s intellectual property and ownership structure form a real, defensible moat. It is not an impenetrable barrier, but it is durable enough to support long-term economic value, strategic optionality, and M&A attractiveness within a realistic commercialization timeframe.

Competitive Moat and Competitive Landscape Analysis

Nature of the Competitive Moat

CARDAMYST’s moat is structural, not molecular. The asset does not win by inventing a new mechanism of action; it wins by integrating a known mechanism with a delivery system, regulatory framing, and care-pathway substitution that collectively change how PSVT is treated. That distinction matters. Competitors do not simply need a drug that works—they need to replicate an entire treatment paradigm.

Clinically, CARDAMYST benefits from mechanistic familiarity. Calcium channel blockade at the AV node is well understood, widely accepted, and trusted by cardiologists and electrophysiologists. This lowers adoption friction relative to novel antiarrhythmics, which often face skepticism and prolonged real-world vetting. At the same time, the intranasal formulation, rapid systemic absorption, short on-off pharmacokinetics, and repeat-dose labeling are not trivial to reproduce. The moat is created by the integration of formulation science, device performance, pharmacokinetics, and labeling—not by chemistry alone.