Porsche AG (P911): Where Engineering Heritage Meets Market Amnesia

A Luxury Franchise Trapped in Cyclical Valuation. Margins at the Bottom, Execution at the Turn. This Is Why the Next Five Years Could Deliver 90 Percent Upside for Patient Capital.

Executive Summary

Porsche AG stands at a cyclical trough that the market has mistaken for structural decline.

The stock has de-rated from its luxury multiple to trade like an industrial cyclical — a misclassification driven by near-term margin compression, China demand weakness, and the heavy cost of its electrification push under Ambition 2030.

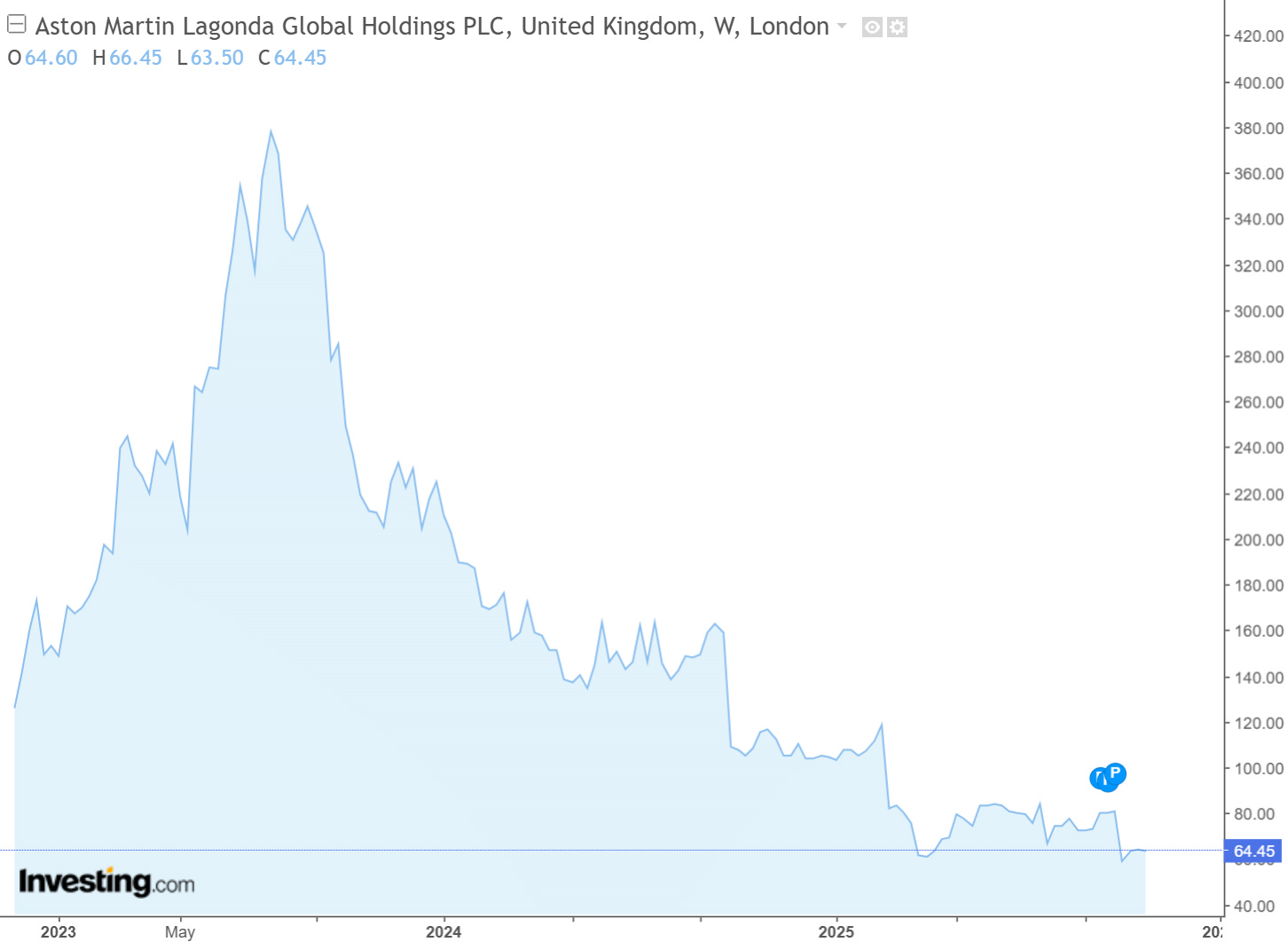

At roughly €47 per share, Porsche now trades on a forward P/E near 20x and trades like Aston Martin — a chronically unprofitable name — and far below Ferrari’s 40x luxury benchmark.

This compression is unjustified. Porsche’s brand equity, cash-generation ability, and product discipline remain intact.

The company’s transition from internal combustion engine (ICE) to battery electric vehicle (BEV) is painful but necessary and controlled: double-capital intensity today, scalable efficiency tomorrow.

My base-case model assumes a restoration of 14–16% operating margins by 2028, supported by €1–1.5 billion of structural cost savings, procurement leverage via Volkswagen Group, and a normalized China contribution.

At a re-rating to 13–15x forward earnings, fair value lands around €70–€75 per share; upside execution pushes toward €90.

Downside to €40 (–15%) remains buffered by hybrids, brand durability, and VW’s industrial scale.

Investment view: Porsche is not broken — it’s misunderstood.

Where others see margin erosion, I see temporary compression before reversion to luxury economics.

The company’s discipline brand elasticity amnd heritage give patient investors asymmetric reward in the next five years.

1. Company Overview

1.1 Brand and Structure

Founded in 1931 and re-listed under Volkswagen Group in 2022, Porsche represents the core profit engine of VW’s premium portfolio.

Unlike most auto brands, its value rests not on volume but on desirability economics — brand scarcity, customization margins, and residual-value trust.

Porsche operates across four main vehicle families:

911 – heritage halo, defining performance identity.

Cayenne / Macan – high-volume, high-margin SUVs.

Panamera / Taycan – GT sedans and BEVs bridging performance and tech.

718 (Boxster / Cayman) – entry-level sports-car platform, moving to full BEV.

Within Volkswagen Group, Porsche contributes roughly 30% of group EBIT on under 5% of volume — underscoring its strategic weight.

1.2 Management & Leadership

Porsche’s leadership structure reflects a deliberate equilibrium between heritage and corporate discipline. The executive team integrates long-standing Porsche managers with VW Group executives, maintaining the brand’s independent engineering ethos while operating within Volkswagen’s industrial and financial oversight.

The company’s governance model remains shaped by the Porsche-Piëch family, whose supervisory influence ensures continuity of brand stewardship. This family presence, paired with VW’s shareholder accountability, provides a rare combination of entrepreneurial flexibility and institutional control — an arrangement that has historically protected Porsche from the short-termism common in the broader auto sector.

In October 2025, CEO Oliver Blume stepped down from his dual role to concentrate fully on leading Volkswagen Group. He will be succeeded by Dr. Michael Leiters on January 1, 2026. Leiters, an engineer by training, brings deep technical and luxury-segment experience, having previously held senior roles at Porsche before serving as Chief Technology Officer at Ferrari N.V. and later as Chief Executive Officer of McLaren Automotive.

This leadership transition signifies more than succession — it marks a shift in operational focus. Blume’s tenure was characterized by strategic expansion, brand management, and record profitability. Leiters’ mandate is execution: to restore double-digit operating returns, deliver disciplined cost efficiency, and prove that Porsche’s electrification strategy can sustain its historical margin profile.

Strategically, management’s direction is defined by three consistent priorities:

Maintain “value over volume.” Porsche will protect brand exclusivity and pricing power even through demand volatility, refusing to chase unsustainable growth.

Accelerate electrification without sacrificing margins. EV rollout will align with cost efficiency, ensuring profitability parity with ICE and hybrid programs by the late 2020s.

Preserve Porsche’s identity through innovation discipline. The company will maintain its engineering DNA and product emotion even as vehicles evolve into software-defined platforms.

Together, these priorities capture Porsche’s leadership ethos — evolutionary, not revolutionary. The firm is not reinventing itself but refining its fundamentals for a new industrial era. Under Leiters’ incoming stewardship, Porsche enters the second phase of its transformation: one where execution replaces narrative, efficiency replaces exuberance, and profitability once again defines performance.

The Problem: Margin Erosion & Market Mispricing

Porsche’s current valuation discount is not rooted in brand weakness or strategic drift, but in a temporary collapse of operating leverage caused by electrification costs, macro headwinds, and geopolitical friction.

The company is suffering the short-term consequences of executing an expensive transition at precisely the wrong point in the global demand cycle. What the market reads as structural decay is, in reality, cyclical compression amplified by sentimental fatigue.

Electrification Cost Burden

The steepest drag on profitability stems from Ambition 2030, Porsche’s commitment to achieve roughly 90 % battery-electric penetration by decade-end.

The parallel rollout of the Taycan and the delayed Macan BEV has created a structural mismatch: heavy R&D expenditure, battery procurement, and factory retooling against still-subscale EV volumes.

Porsche is effectively running two industrial cost bases — mature ICE / PHEV platforms that fund operations, and a nascent BEV ecosystem that demands massive upfront capital. This “double-capital intensity” has inflated depreciation, squeezed gross margin, and temporarily destroyed operating leverage.

Unlike mass-market peers that can amortize BEV cost faster, Porsche’s low volume and high engineering complexity magnify early inefficiencies. The result: operating returns have fallen from the historical 15–17% range to mid-single digits, even as revenue remains resilient. Yet the logic is deliberate. By retaining ICE and hybrid production during the transition, Porsche self-funds its electrification rather than relying on debt or dilution — short-term pain to secure long-term independence.

Weakness in China and Global Demand Softness

China — once Porsche’s most reliable profit engine — has become its largest vulnerability. The combination of economic slowdown, property-market deflation, and consumer retrenchment has eroded demand for imported luxury performance vehicles. Deliveries are down double digits year over year, and the mix has shifted toward lower-trim models with fewer bespoke options, directly cutting per-unit margin.

Domestic competitors such as BYD (YangWang), NIO, Zeekr, and Xiaomi have captured affluent younger buyers by emphasizing technology, range, and connected-vehicle features — areas where Porsche is still scaling up. The result is pricing rigidity: Porsche refuses to discount, preserving brand equity, but at the cost of volume flexibility.

Outside China, higher global interest rates and inflation have muted discretionary spending. In the United States, premium auto financing costs remain near decade highs; in Europe, energy inflation has dented household confidence. Even loyal customers are deferring purchases or opting for lower-spec trims, compressing Porsche’s once-predictable option-attachment revenue.

The brand’s “value-over-volume” ethos prevents oversupply — but it also limits responsiveness in a cyclical downturn. Until macro conditions normalize, the company must rely on strict cost control and hybrid stability to offset top-line softness.

Tariffs, Supply Chain, and Input-Cost Inflation

Geopolitics has added a new layer of cost volatility. Tariff escalation between the U.S., EU, and China increases landed costs on German-built 911 and Cayenne exports by roughly +250–300 bps, while 2024’s Red Sea rerouting and Asia-lane constraints imposed additional logistics pressure (route-dependent, but broadly +10–30% on freight), worth roughly –10 to –20 bps of EBIT drag. Because Porsche prioritizes value over volume, it has chosen not to chase price offsets aggressively; the brand absorbs a meaningful share of these shocks to protect long-term pricing integrity and residual values.

On inputs, the picture is deliberately uneven—just as in your table:

Lithium carbonate (€/t): ~€70,000 → ~€10,000 from 2022 to 2024, a collapse of roughly –85%. This is a tailwind to pack costs and contributes about +20 to +40 bps to EBIT once inventory and contracts roll through.

Semiconductors (per-vehicle cost proxy): up ~+19% vs 2022 (or ~+24% vs 2021), equating to roughly –30 to –40 bps EBIT impact given higher chip density in BEV architectures.

Aluminium (LME, €/t): ~€2,473 → ~€2,200, essentially flat to –10% versus 2022, a small –0 to –10 bps headwind after energy surcharges and processing pass-throughs.

Nickel (LME, €/t): ~€23,000 → ~€16,000, down –30 to –35%, a modest +5 to +10 bps tailwind as cathode mix and supplier terms reset.

Ocean freight (Asia–EU lanes): +10–30% vs 2022 during the 2024 disruption window, worth –10 to –20 bps on mix-weighted exports.

etting these forces, materials deflation is no longer the core constraint; the real near-term drag lies in policy-driven tariffs and architecture-driven semiconductor intensity during the BEV ramp.

In fact, the incoming 2026 911 lineup underscores this dynamic: the base Carrera now starts at roughly US $129,950, representing a near-7 % increase year-over-year.

Meanwhile, the new 911 Turbo S hits US $272,650 for the coupe and ~US $286,650 for the convertible, placing it squarely in super-car pricing territory despite being an iteration of the “core” sports-car brand.

These numbers matter because they illustrate the commercial tension: Porsche is absorbing rising fixed costs — advanced chassis electronics, hybrid/tracked powertrain updates, semiconductor content — while refusing to compromise on luxury pricing or resort to discounting. That discipline protects long-term margins but necessarily prolongs the cyclical bottom. It contributes why 2025 is modelled as the trough year: until the architecture resets (software, IP, BEV modularisation) and batch economies kick in, Porsche accepts mid-single-digit returns. Once those reforms hit, procurement leverage and volume scale should lift RoS back toward the low-teens.

2025 Guidance Reset

Cumulatively, these pressures forced management to issue a sharp profitability downgrade.

For 2025, Porsche guides to an operating return on sales ( RoS ) of 5–7% and near-breakeven free cash flow — its weakest outlook in over a decade. For the first time, Porsche will earn less per vehicle than Toyota or Hyundai.

This revision is a strategic reset, not capitulation. Management has openly defined 2025 as the “trough year,” clearing the decks for cost-reduction implementation and BEV scale ramp from 2026 onward. Once procurement savings and BEV utilization rates begin to flow through, RoS is expected to recover into the low-teens by 2027 and normalize near 15% by 2028.

In capital-cycle terms, Porsche is effectively absorbing its depreciation front-loaded — taking the write-off today to rebuild efficiency tomorrow.

Market Overreaction and Valuation Compression

The equity market has reacted with blunt pessimism.

Porsche now trades near 20x forward P/E, its share prices trades like Aston Martin (AML) — a luxury auto maker that has struggled for decades to sustain profitability — and at roughly half Ferrari’s 40x multiple. This parity is irrational. Investors have conflated transitory cost absorption with structural impairment.

The market’s current pricing implies that Porsche will never regain double-digit margins — an assumption inconsistent with both its history and its operating model. Even partial margin normalization to 12–14% would justify a re-rating into the 13–15x band, delivering 50–90% upside from current levels.

By contrast, downside risk remains defined: hybrids and VW backing create a hard floor near €40. The asymmetry is evident — limited downside, open-ended upside as sentiment and profitability converge.

The Core Disconnect

The underlying issue is valuation distortion, not business decay.

Porsche remains structurally profitable, brand-resilient, and cash-generative. What has changed is investor perception: the company has been re-categorized from a luxury franchise to an industrial cyclical.

This misclassification stems from short-term earnings optics rather than long-term economics. The electrification cycle has temporarily compressed return on sales, but the brand’s pricing power, product elasticity, and cost-reduction roadmap remain largely intact.

In essence, Porsche’s current trading level represents a textbook turnaround mispricing — where short-term pessimism suppresses long-term intrinsic value. As the cost-reform program gains traction and BEV margins close the gap with ICE, sentiment will inevitably revert.

For contrarian investors, this disconnect defines the opportunity: Porsche’s fundamentals are cyclical, not secular. The company’s challenge is execution timing, not existential viability.

3. The Turnaround Plan

Porsche’s recovery strategy is neither reactive nor experimental. It is a structured bridge — designed to navigate a profitability trough, not to reinvent the brand (unlike Jaguar Land Rover).

Management’s plan rests on three synchronized pillars:

(1) cost optimization and structural efficiency,

(2) strategic power train diversification, and

(3) disciplined electrification rollout.

Together, these initiatives aim to rebuild double-digit operating margins by 2028 and re-establish Porsche as Volkswagen Group’s margin anchor. The company explicitly defines 2025 as the bottom of its cycle, with a multi-year normalization path anchored in operational execution rather than volume expansion.

Cost-Cutting and Structural Efficiency (€1–1.5 Billion Savings Target)

At the center of Porsche’s turnaround lies a multi-phase efficiency program targeting €1–1.5 billion in structural savings from 2026 onward. The focus areas include procurement reform, production optimization, workforce realignment, and digital integration — each directly addressing cost inflation and scale inefficiency caused by the EV transition.

Procurement Reform:

Roughly half of the targeted savings will come from consolidating supplier networks and leveraging Volkswagen Group’s global purchasing power. Battery components, semiconductors, and aluminum are key categories where Porsche can benefit from VW’s shared scale — reducing per-unit material costs and stabilizing supply.

Manufacturing Efficiency:

Porsche is upgrading its Leipzig and Zuffenhausen plants to support platform flexibility, enabling shared production between ICE, PHEV, and BEV vehicles on modular lines. This transition toward automation and flexible architecture is expected to reduce fixed-cost intensity by 15–20% by 2027.

Workforce and Process Optimization:

While Porsche avoids mass layoffs, natural attrition and selective restructuring will align headcount with digital workflows. Back-office and non-core functions are being digitized through ERP upgrades and predictive manufacturing analytics — driving long-term labor productivity gains.

The guiding philosophy is clear: margin protection without brand dilution. Porsche refuses to sacrifice product exclusivity for cost savings. Instead, it seeks to restore profitability by structurally lowering its cost-to-revenue ratio while maintaining premium pricing power. The program mirrors the kind of margin discipline more common to high-end industrials than automakers.

Extending ICE and PHEV Models to Protect Margins

Acknowledging that full electrification will take longer than once forecast, Porsche has chosen pragmatism over ideology. The company is extending the life of its internal combustion (ICE) and plug-in hybrid (PHEV) models — notably the Cayenne and Panamera — to serve as high-margin cash bridges during the EV ramp.

These hybrids, particularly the Cayenne Turbo E-Hybrid, remain among the most profitable vehicles in the portfolio. They generate the free cash flow needed to fund BEV development while maintaining Porsche’s hallmark performance identity and emissions compliance.

This dual-track strategy provides two key advantages:

Cash Flow Stability: Hybrid sales sustain capital efficiency, preventing the need for external financing during EV scale-up.

Regional Adaptability: Markets with slow EV adoption — such as the Middle East, Southeast Asia, and parts of the U.S. — will continue to demand hybrids, ensuring balanced global revenue streams.

By avoiding a hard pivot away from ICE, Porsche minimizes execution risk and prevents the “EV cliff” that has destabilized peers. It also ensures brand loyalty during a period when infrastructure, consumer readiness, and regulatory frameworks remain inconsistent across regions.

The BEV Rollout Roadmap: Macan BEV and 718 BEV

Porsche’s electrification strategy has evolved from speed to sequencing. Rather than front-loading model launches, the company is now executing a disciplined rollout designed to balance innovation with capital efficiency.

The next major step is the Macan BEV, scheduled for global scaling through 2026. Built on the new PPE (Premium Platform Electric) architecture co-developed with Audi, it represents Porsche’s first attempt to replicate its SUV success formula in a fully electric format. Targeted at Europe, China, and North America, the Macan BEV aims to achieve the performance credibility of the Taycan with improved range, manufacturability, and cost efficiency.

Following that, the 718 BEV (successor to the Boxster/Cayman) anchors Porsche’s second EV wave. As the brand’s first lightweight electric sports car, it embodies Porsche’s core design ethos — performance through precision, not excess. With a compact, mid-motor architecture and advanced cell chemistry, the 718 BEV is expected to deliver a margin uplift versus the first-generation Taycan once production scales.

This staggered rollout marks a deliberate break from the “growth-first” Taycan era. By spacing launches and sharing battery platforms across VW’s premium brands, Porsche reduces capital overlap, optimizes supplier capacity, and smooths R&D amortization — all of which support free cash flow recovery.

Expected Margin Recovery Timeline (2026–2028)

Porsche’s path to recovery follows a disciplined, three-phase progression — designed not around aggressive growth targets, but around the systematic restoration of profitability and capital efficiency. The company’s strategy deliberately sequences restructuring, cost optimization, and EV scaling in a way that preserves brand integrity while rebuilding its operating leverage.

The process begins with Phase I: Stabilization (2025–2026), which marks the low point of the margin cycle. Here, Porsche focuses squarely on cost control and internal recalibration. Restructuring measures and the initial tranche of procurement reforms begin to flow through, while ICE and hybrid models act as cash flow anchors. The operating return on sales (RoS) during this phase is expected to remain subdued at 5–8%, reflecting continued headwinds from electrification investment and macro softness. Yet, this period lays the operational groundwork for recovery — reducing structural inefficiencies, cutting redundant spend, and eliminating one-off charges that have distorted earnings quality.

The second stage, Phase II: Inflection (2026–2027), represents the turning point. By mid-2026, the Macan BEV begins ramping to scale, leveraging shared platforms and component efficiencies within the Volkswagen ecosystem. Procurement savings begin to compound, factory utilization improves, and R&D amortization begins to normalize. Margins are expected to rise into the 9–12% range, signaling the first tangible proof that Porsche’s electrification can coexist with profitability. This phase coincides with the full activation of the €1–1.5 billion cost-saving program — transforming the operating model from capital-heavy to efficiency-driven.

Finally, Phase III: Expansion (2027–2028) completes the turnaround cycle. The 718 BEV enters production, serving as both a brand and margin catalyst. As BEV programs reach maturity, production scale and pricing power reinforce each other: unit economics improve, fixed costs flatten, and optionality returns to the product mix. Operating returns are projected to normalize within the 13–16% corridor, effectively re-establishing Porsche’s historical margin leadership. This marks a structural—not cyclical—return to profitability, underpinned by a leaner cost base and more diversified powertrain portfolio.

By 2028, Porsche expects to operate once again as a high-return luxury franchise — but with a more flexible cost structure, lower break-even point, and greater resilience to input volatility. The recovery blueprint assumes a moderate macro stabilization, easing commodity pressures, and sustained execution discipline.

Even throughout this trough period, Porsche’s management has refused to engage in aggressive discounting — a critical signal of confidence in brand equity and long-term pricing power. This restraint will prove accretive once demand normalizes: every avoided discount today preserves future pricing headroom and accelerates operating leverage when volumes rebound.

In sum, Porsche’s recovery is not a rebound built on optimism, but a re-engineering of its earnings architecture. Each phase compounds operational efficiency and scale synergy, paving the way for a full margin normalization cycle that restores Porsche’s standing as the most profitable full-line automaker in the world.

Financial Outlook & Valuation

Porsche’s next five years will define the bridge between cyclical compression and structural normalization.

The company enters 2025 at a profitability trough — burdened by electrification costs, tariff pressure, and China weakness — yet it also begins to execute on a credible recovery roadmap.

The combination of cost reform, disciplined BEV rollout, and a gradual macro rebound sets the stage for a multi-year re-rating, both operationally and in market perception.

Profitability Trajectory (2025–2030)

Porsche’s financial trajectory reflects a measured climb from trough-level profitability toward margin restoration by the decade’s end.

Revenue is projected to rise from approximately €37.5 billion in 2025 to €50 billion by 2030, representing a compound annual growth rate of roughly 6.5%.

The near-term headwinds of 2025 — down roughly 6–7% year over year — will give way to sequential recovery beginning 2026, driven by new BEV launches and mix normalization.

Gross margin is expected to recover from 25% in 2025 to around 33% by 2030, supported by procurement efficiency, automation gains, and scale benefits from Volkswagen Group’s platform-sharing model.

Operating margins (EBIT return on sales) follow a similar trajectory, improving from 5% at the trough to 8% in 2026, 12% in 2027, and 14–16% by 2028–2030.

This progression effectively re-establishes Porsche’s historical profitability corridor, restoring it to its status as the most profitable full-line automaker in Europe.

Operating profit expands accordingly — from €1.9 billion in 2025 to €8.0 billion by 2030, marking more than a fourfold increase in operating earnings across the period.

Net margins follow this path, widening from 3% to roughly 11%, translating into net income growth from just over €1 billion in 2025 to €5.5 billion by 2030.

Free cash flow — the lifeblood of Porsche’s investment flexibility — rises from €0.7 billion in 2025 (a mere 2% FCF margin) to over €5 billion, representing 10% of revenue by the end of the decade.

From a balance sheet perspective, leverage steadily declines as cash generation improves.

Debt-to-EBITDA falls from 2.8x in 2025 to 1.0x by 2030, underscoring management’s commitment to maintaining conservative capital discipline throughout the transition.

As efficiency gains take hold, valuation multiples should compress structurally — EV/EBITDA is expected to decline from 9x to around 6x, signaling higher cash conversion and lower capital intensity.

This trajectory translates to a clear equity path: Porsche’s implied share value rises from the current €47 to roughly €55 by 2026, €65 by 2027, €75 by 2028, and €90 by 2030, reflecting cumulative upside of ~90% from current levels if the turnaround proceeds as planned.

Scenario Framework

Porsche’s valuation case hinges on three distinct execution scenarios — downside, base, and upside — reflecting the sensitivity of margins and multiples to electrification timing and macro conditions.

Downside Case

Margins stagnate below 10% as EV transition costs persist longer than expected and China demand remains sluggish.

This scenario assumes only partial realization of the €1–1.5 billion cost-savings target and continued input inflation.

Under those conditions, Porsche would likely be valued at 10–12x forward earnings, implying a fair value near €40 per share, or about 15% downside from today’s levels.

Even here, the company remains profitable, with balance-sheet strength and hybrid cash flow preventing any structural impairment.

Base Case

Represents the most probable outcome, assuming gradual but steady normalization.

Porsche successfully executes its efficiency program, restores operating margins to 14% by 2028, and achieves solid BEV economics as the Macan and 718 EVs reach scale.

Revenue expands at a mid-single-digit rate, supported by stable SUV demand and selective pricing power.

In this scenario, valuation re-rates to 13-14x forward earnings, consistent with re-valued European premium peers such as BMW and Mercedes-Benz.

The implied equity value is approximately €70 per share, representing ~50% upside from the current €47 base.

Bull Case

Porsche executes flawlessly.

Operating margins surpass 16%, electrification scales faster than anticipated, and Chinese demand stabilizes alongside global monetary easing.

As Porsche reclaims its luxury identity, the market re-rates the company back toward 15–16x forward P/E, in line with historical luxury peers.

That valuation supports a €90 per share target, equating to nearly 90% upside within a 4–5 year horizon.

In this scenario, Porsche would effectively complete its transformation into a leaner, more capital-efficient luxury brand — with cost structure improvements permanently embedded in its model.

Valuation Dynamics and Peer Context

At current prices, Porsche trades near 20x forward earnings, an anomaly in context.

It sits between cyclical automakers (BMW ~11x) and high-end luxury peers (Ferrari ~40x), effectively punished for being both an automaker and a luxury franchise — a hybrid classification that fails to capture its true earnings power.

The market’s implicit assumption is that Porsche’s margin recovery will stall permanently, keeping it trapped below 10%.

If this assumption proves false, the equity offers asymmetrical reward: even a partial re-rating to the 13–15x range as margins stabilize would unlock substantial upside.

Viewed through a cash flow lens, the case strengthens. At a normalized FCF yield of 7–8%, Porsche offers one of the most attractive risk-adjusted return profiles among European industrials — combining dividend support, tangible asset coverage, and a credible multi-year re-rating story.

This profile makes Porsche both a value recovery and a structural compounding play, depending on investor horizon.

Re-Rating Catalysts

Several near-term triggers could drive sentiment reversal and valuation recovery between 2025 and 2028:

Execution Proof: Confirmation that cost savings and margin expansion are tracking to plan, particularly in the FY2026 and FY2027 results.

BEV Credibility: Successful Macan BEV and 718 BEV ramp, demonstrating that Porsche can scale electrification without compromising profitability.

China Stabilization: A rebound in Chinese discretionary demand or tariff moderation improving export margins.

Tariff Resolution: Any de-escalation in EU–U.S.–China automotive tariffs immediately expands Porsche’s export EBIT leverage.

Investor Reclassification: Restoration of Porsche’s inclusion in European luxury and ESG indices as margins exceed 12% again.

Together, these catalysts form the basis for sentiment re-rating — shifting the market view from cyclical stress to operational resilience.

Valuation Synthesis

In summary, Porsche’s equity today trades at a level that prices in a permanent impairment to its margin structure.

Yet, its strategic positioning — high brand equity, integrated VW scale, and disciplined capital stewardship — points instead toward gradual normalization and re-rating.

The base case of €70 per share offers compelling asymmetry: minimal downside (–15%) anchored by strong free cash flow and tangible asset backing, versus potential 90% upside as profitability converges back toward historical norms.

For long-term investors, Porsche represents a rare instance where luxury brand economics intersect with cyclical valuation despair — a setup that historically rewards patience.

If management executes on cost, mix, and electrification as planned, Porsche’s recovery will not merely restore margins; it will redefine the economics of performance luxury in the EV era.

Risks & Mitigation

Every turnaround depends not only on the depth of the problem but on the durability of its defenses. Porsche’s recovery narrative is credible but not without risk. Execution across cost control, BEV rollout, and global demand normalization must align to restore the brand’s structural profitability. The following outlines the principal risks — and the mechanisms by which Porsche’s management and group structure mitigate them.

Key Risks

1. EV Transition Delays

The largest execution risk lies in the pace and profitability of Porsche’s electric transition. Scaling production of the Macan BEV and 718 BEV depends on battery chemistry readiness, supplier reliability, and software integration. Any delay in ramp or software instability could defer Porsche’s margin inflection timeline, keeping RoS below 10 % for longer than planned. A prolonged mismatch between EV cost and pricing power would weaken near-term free cash flow and extend the valuation overhang.

2. China Demand Weakness

China remains Porsche’s most important single market, representing roughly one-third of global deliveries and an outsized share of profit mix. The macro environment — defined by slowing consumption, rising local competition, and import tariffs — continues to weigh on premium car demand. Prolonged weakness could compress pricing power, particularly for SUVs, which historically carry Porsche’s highest per-unit margins.

3. Tariffs and Trade Friction

Geopolitical risks remain structurally embedded in Porsche’s export model. Tariff escalation between the EU, the U.S., and China could further inflate landed costs for core models like the 911 and Cayenne. With production concentrated in Germany, Porsche has limited geographic flexibility in the near term. Trade disruptions or retaliatory duties could erode 40–60 basis points of operating margin per incremental 5% tariff escalation.

4. Input-Cost Inflation

Though commodity prices have moderated, volatility in aluminum, nickel, and semiconductor supply continues to pose risk. Structural inflation in high-tech components and logistics adds pressure on BEV cost structures, which are already margin-dilutive. If raw material normalization stalls, the company’s €1–1.5 billion savings target could face headwinds, deferring Porsche’s intended margin expansion by one to two fiscal years.

5. Execution Fatigue

Porsche’s turnaround depends on sustained management execution amid concurrent leadership change — with Dr. Michael Leiters assuming CEO responsibilities in 2026. Transition periods introduce uncertainty, particularly when legacy initiatives must overlap with new strategic direction. If execution focus wavers, investor patience could erode even before financial recovery manifests.

Mitigation Factors

1. Brand Equity and Pricing Power

Porsche remains one of the strongest luxury marques globally — its brand elasticity allows it to maintain premium pricing through downturns. Customer loyalty, limited edition models, and high option-attach rates provide a natural hedge against volume volatility. Even during 2024–2025, Porsche has resisted discounting, ensuring long-term brand durability and residual-value protection.

2. Cost-Reduction and Efficiency Program

The €1–1.5 billion structural savings plan forms the backbone of Porsche’s resilience. Procurement consolidation, manufacturing automation, and digital integration across the Leipzig and Zuffenhausen plants provide tangible levers to offset inflationary pressure. These initiatives are not cyclical cost cuts but permanent structural efficiencies that will improve long-term operating leverage.

3. Volkswagen Group Integration

Porsche’s position within the Volkswagen ecosystem gives it scale advantages that pure-play luxury peers lack. Shared R&D, battery supply, and digital platform investments reduce capital intensity, while VW’s financial backing ensures liquidity even in extended downturns. This group integration provides strategic insulation from macro shocks and ensures supply-chain redundancy across critical components.

4. Flexible Powertrain Strategy

Unlike luxury EV start-ups or one-dimensional legacy transitions, Porsche’s dual-track approach — maintaining ICE and hybrid lines alongside BEVs — protects short-term profitability and cash flow. This flexibility allows the company to tailor its mix by region, maintaining earnings stability while gradually expanding its electrified portfolio. In emerging markets or regions with slower infrastructure rollout, hybrids will remain key profit bridges.

5. Managerial Continuity and Governance Stability

Despite upcoming leadership change, governance stability remains anchored by the Porsche-Piëch family’s supervisory presence and Volkswagen Group oversight. This dual structure balances long-term brand stewardship with financial accountability. The incoming CEO’s technical pedigree and luxury-brand experience mitigate the risk of strategic drift, ensuring continuity through the transition.

Risk-Reward Summary

In aggregate, Porsche’s risk profile is one of timing, not structural fragility. The key question is not whether profitability returns, but how soon — and how strongly. The company’s brand durability, cost discipline, and VW integration provide natural shock absorbers that limit downside even in adverse scenarios. Meanwhile, the asymmetry of outcomes remains compelling: limited erosion potential against a sharply positive re-rating path once execution milestones are met.

For investors, the calculus is straightforward: Porsche’s recovery risk is operational, not existential. Its valuation, however, still reflects the latter. The company’s ability to prove consistent cost execution, margin traction, and BEV scalability will determine the pace of revaluation — but not its inevitability.

Investor Takeaway

Porsche’s sell-off reflects cyclical fear, not structural decline. The market is treating a temporary investment phase as permanent impairment — valuing one of the world’s strongest automotive franchises like a mid-cycle industrial. In reality, Porsche’s margin erosion is a by-product of its Ambition 2030 electrification drive, front-loaded costs, and short-term China weakness — all reversible conditions within a two-to-three-year window.

The turnaround framework is credible: €1–1.5 billion in structural cost savings, disciplined BEV rollout sequencing (Macan BEV → 718 BEV), and hybrid cash-flow bridges that sustain profitability through transition. Execution risk exists, but the roadmap is coherent, capital-light, and underpinned by Volkswagen’s scale. By 2028, operating margins should normalize back to 14–16%, restoring Porsche’s status as VW Group’s profit anchor and Europe’s most efficient full-line luxury automaker.

At roughly €47 per share, the market prices Porsche as though margins will never again exceed 8%. The base case of €70 implies 50% upside; the upside scenario of €90 implies near-doubling potential as re-rating follows margin restoration. Downside remains limited by tangible assets, hybrid cash generation, and VW backing.

For contrarian investors, Porsche offers a classic asymmetric setup: short-term pain, long-term leverage. The stock is no longer priced for excellence — it’s priced for mediocrity. If management delivers even a modest portion of its turnaround plan, the next few years could mark one of the most significant profitability recoveries in Europe’s premium auto space.

In short: this isn’t a broken company — it’s a mispriced franchise. Porsche’s brand endurance and cost discipline make it a rare opportunity where cyclical pessimism meets structural quality.

Disclaimer, Disclosure, Conflicts & Copyright Notice

This publication has been prepared solely for informational and educational purposes by Alpha Talon Investment Research (“Alpha Talon”). The views expressed herein represent the author’s independent analysis and opinions as of the date of writing and may change without notice. This material does not constitute investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security, derivative, or financial instrument. Nothing contained in this document should be construed as an offer to sell or a solicitation to buy any securities.

Investing in securities involves significant risk, including the possible loss of principal. Equity investments may fluctuate in price, sometimes dramatically. Securities in the biotechnology, pharmaceutical, oncology, and healthcare sectors—such as those discussed herein—are subject to heightened levels of clinical, regulatory, competitive, and operational risk. Forward-looking statements, projections, price targets, valuation scenarios, and estimates included in this report are inherently speculative, based on numerous assumptions, and may differ materially from actual outcomes. Past performance is not indicative of future results.

This material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research produced by broker-dealers or regulated financial institutions. This document is not a research report under FINRA, SEC, FCA, or MiFID II definitions. It has not been reviewed, endorsed, or approved by any regulatory authority, including FINRA, the SEC, or any similar body. Alpha Talon is not a registered investment adviser, broker-dealer, or financial institution under SFC or MPFA.

Readers should conduct independent research and due diligence before making any investment decision. You should consult a licensed investment adviser, registered financial professional, tax specialist, or attorney regarding your specific financial situation and risk tolerance. Nothing in this publication establishes any fiduciary relationship, advisory relationship, or obligation on the part of the author or Alpha Talon toward any reader.

The author and affiliated accounts may hold long or short positions in the securities and financial instruments discussed in this report and may trade in them before, during, or after publication without further notice. These positions may be contrary to the views expressed herein. The author does not receive compensation from the issuers of any securities mentioned. Alpha Talon does not have investment banking relationships, commercial relationships, consulting arrangements, or compensation agreements with the companies discussed in this document.

No part of the author’s compensation is directly or indirectly related to the specific recommendations, analyses, or opinions expressed in this report.

All investments involve risk, including loss of principal. Certain securities discussed may be speculative or volatile and may not be suitable for all investors. Clinical trial failures, regulatory decisions, market conditions, macroeconomic shifts, geopolitical developments, and competitive pressures can significantly impact the securities analyzed. This information is provided “as is,” without warranty of any kind, express or implied.

Securities mentioned herein are not guaranteed, not insured, and not protected by SIPC except as applicable for brokerage custody, and are not obligations of, or guaranteed by, any bank or government agency.

Alpha Talon, its author(s), and affiliates expressly disclaim all liability for errors, omissions, or any direct, indirect, incidental, or consequential losses arising from the use of this material. Use of the information is at the reader’s sole risk.

This material may not be distributed or used in any jurisdiction where such use or distribution would be contrary to local law or regulation. Readers are responsible for complying with applicable securities laws.

For paid subscribers, please find our report for Porsche AG (ETR: P911 | OTCMKTS: POAHY) below, its 34 pages of comprehensive analysis of Porsche AG.

As per for multi-listed equities, the executive summary is in both Englished and German/Deutsch, there might be some translation issues, if there are any translation issues, please reachout.

For free subscribers the report will be available after an one month delay!